30:18 (1X)

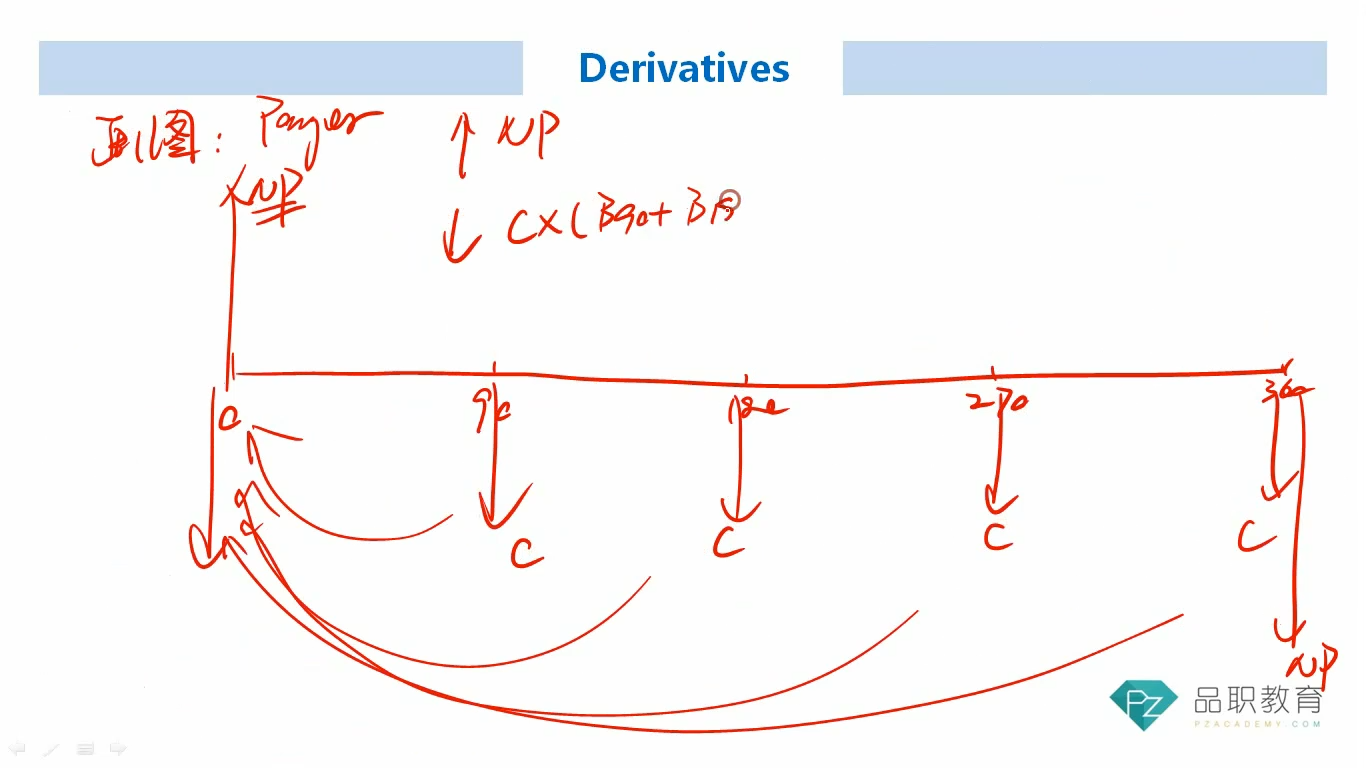

Why is the up arrow for notional principal at time 0, shouldn't it be at time 360 days?

pzqa35 · 2023年10月11日

嗨,努力学习的PZer你好:

This section discusses the pricing of the interest rate swap. Payer swap means that I will pay a fixed interest rate and receive a floating interest rate. As the teacher mentioned earlier, for a floating interest rate bond, its value will return to the face value at each reset node. Therefore, at time 0, the value of the floating bond I receive is equal to the face value, and the value of the fixed interest rate bond paid is equal to the sum of discounted future cash flows. Swap, like forward, has a value of 0 at time 0, so the received value is equal to the value of the expenditure, and thus the fixed swap rate is calculated.

----------------------------------------------努力的时光都是限量版,加油!