NO.PZ2023041003000041

问题如下:

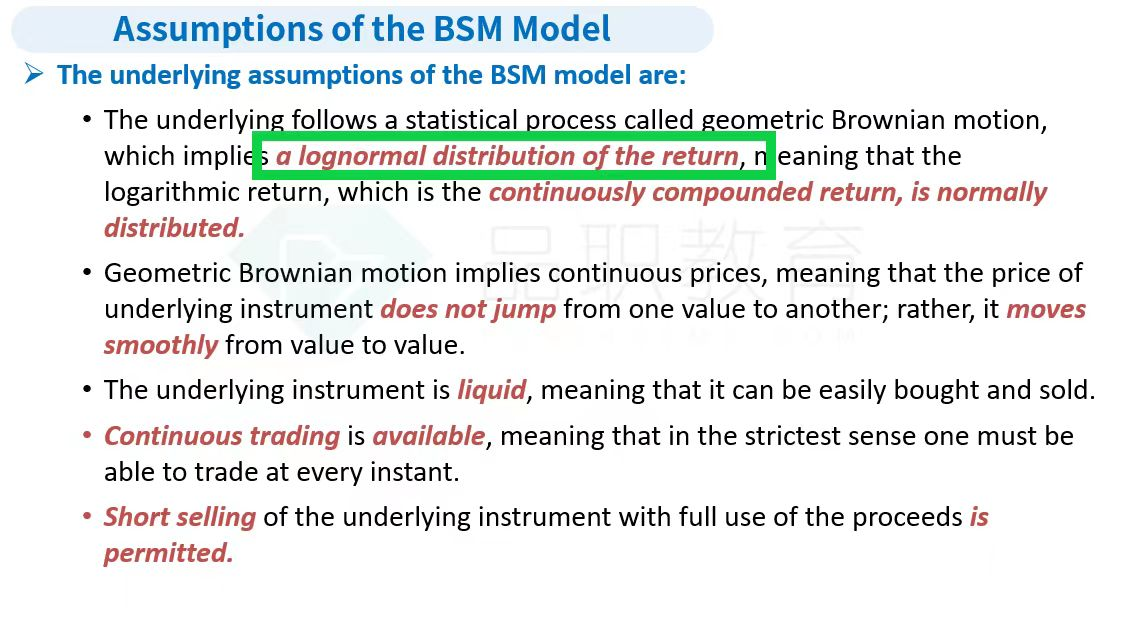

Lee begins: “We use the Black-Scholes-Merton (BSM)

model for option valuation. To fully understand the BSM model valuation, one

needs to understand the assumptions of the model. These assumptions include

normally distributed stock returns, constant volatility of return on the

underlying, constant interest rates, and continuous prices”

Lee’s statement about the assumptions of the BSM

model is accurate with regard to:

选项:

A.

interest rates but not continuous prices.

B.

continuous prices but not the return distribution.

C.

the stock return distribution but not the volatility.

解释:

Although the BSM model assumes continuous stock

prices, it also assumes that stock returns are lognormally distributed (not

normally distributed).

股票收益可正可负,不就是正态分布吗?股票价格只能是正的,才是lognormal