NO.PZ2023041003000021

问题如下:

Johnson prices a three-year Libor-based interest

rate swap with annual resets using the present value factors presented in

Exhibit 1.

Exhibit 1 Present Value Factors

Johnson also uses the present value factors in

Exhibit 1 to value an interest rate swap that the bank entered into one year ago

as the receive-floating party. Selected data for the swap are presented in

Exhibit 2. Johnson notes that the current equilibrium two-year fixed swap rate

is 1.12%.

Exhibit 2 Selected Data on Fixed for Floating Interest Rate Swap

From

the bank’s perspective, using data from Exhibit 1, the current value of the

swap described in Exhibit 2 is closest to

选项:

A.

-$2,951,963.

B.

-$1,849,897.

C.

-$1,943,000.

解释:

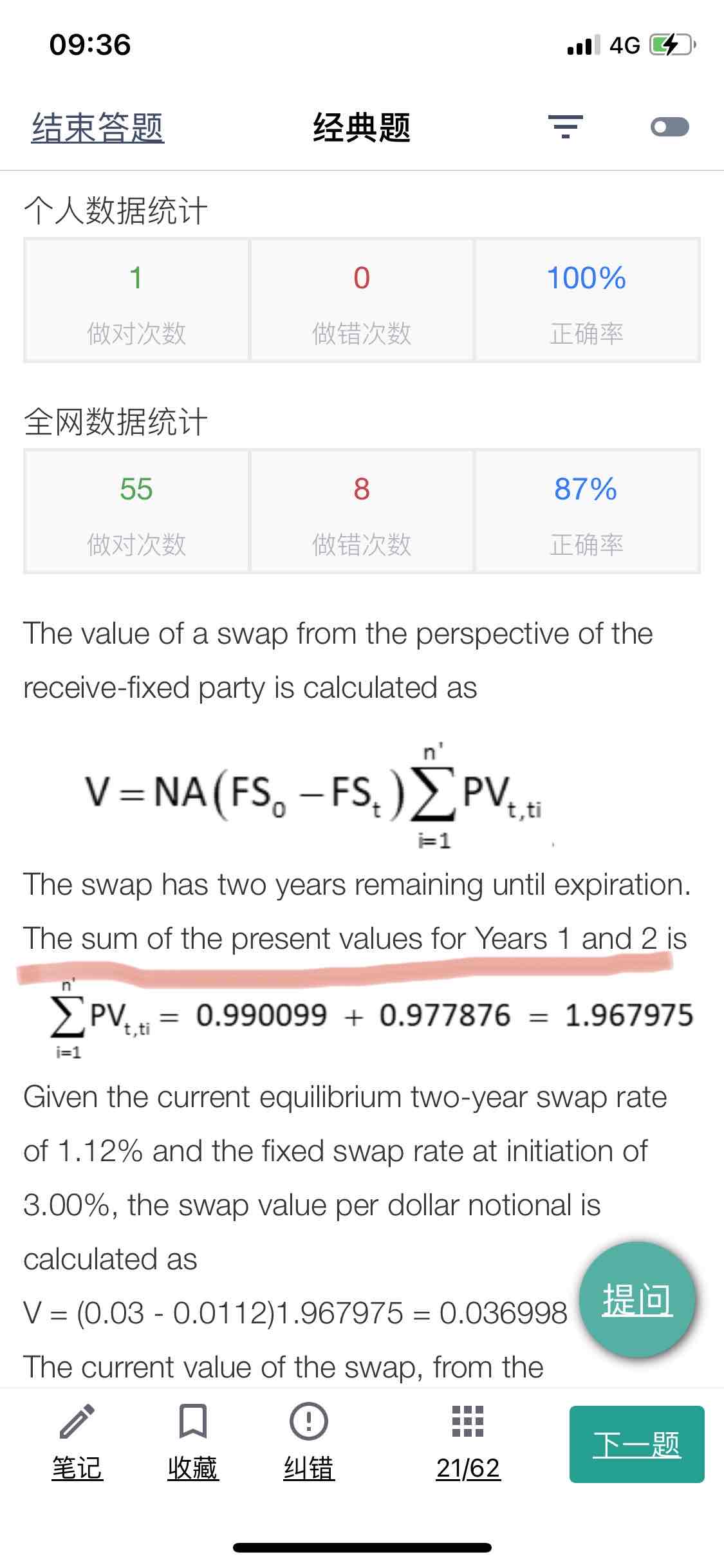

The value of a swap from the perspective of the receive-fixed party is

calculated as

The swap has two years remaining until expiration. The sum of the

present values for Years 1 and 2 is

Given the current equilibrium two-year swap rate of 1.12% and the fixed

swap rate at initiation of 3.00%, the swap value per dollar notional is

calculated as

V = (0.03 -

0.0112)1.967975 = 0.036998

The current value of the swap, from the perspective of the receive-fixed

party, is $50,000,000 x 0.036998 = $1,849,897.

From the perspective of the bank, as the receive-floating party, the

value of the swap is -$1,849,897.

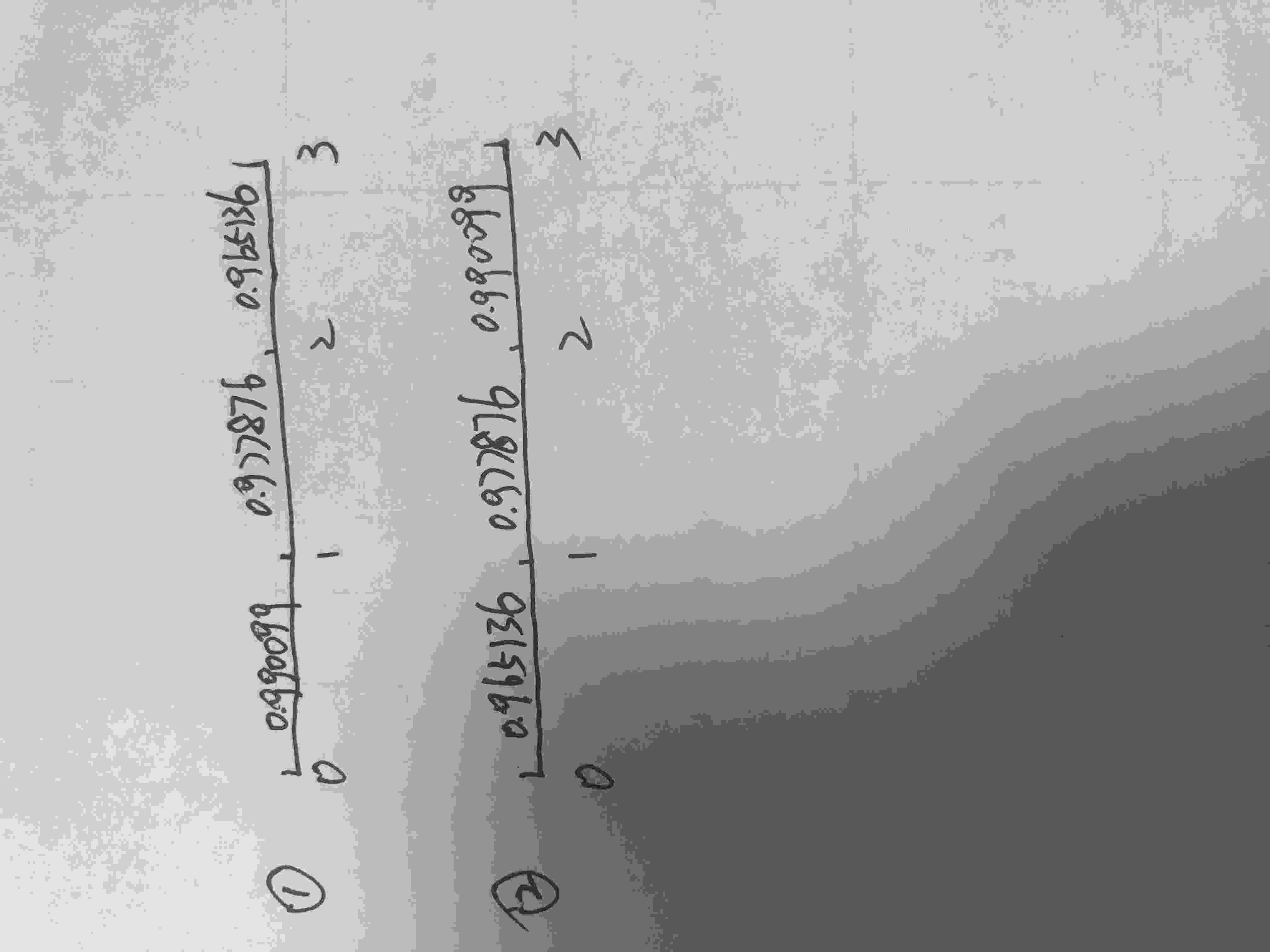

1.画时间轴的话,折现因子归属到底是哪种?我认为应该是1,时间越长利率越高,折现因子就越小,0.965136应该对应第三年。

2.现在是站在1这个时间点,还有两年到期,算PV的和不应该是第2年和第3年的和吗?怎么会是第1年和第2年,把前两年的和加一起最后站在的不是2时间点吗?