发亮_品职助教 · 2018年06月08日

Riding the yield curve要成功,需满足以下条件:

1. 收益率曲线upward-sloping,(意思就是forward rate大于spot rate,且forward rate是upward-sloping的)

2. 收益率曲线stable,这个stable是指,今年收益率长什么样,明年还长什么样;你也可以预测5年内,10年内,收益率曲线stable,我们简便讨论就预测明年的一样。

3. 债券maturity大于investment horizon。

这个道理其实就是:upward sloping的spot rate,说明当前forward rate高于当前spot rate,如果策略实施者预测未来spot rate和当前spot rate一样,那么就是在策略实施者眼里认为未来的spot rate低于当前市场的forward rate;

即,在策略实施者眼里,一年过去后,未来现金流的折现率,是低于当前市场价格里用到的forward rate的折现率的。

所以在他眼里,1年过去后,由于收益率曲线不变(没有实现市场预期的forward rate),所以他认为折现率更低,他认为债券价格的应该更高,如果不是持有至到期,提前卖出可以获得capital gain。

举个例子:

如下图,已知 1-year spot rate是2%;2-year是4%,3-year是7%;4-year是9%;

从spot rate可以求出来forward rate;

f(1,1)=6.04%;f(1,2)=9.59%;f(1,3)=11.44%

假设投资期只有1年,我们买一个1-year zero coupon bond,那么我们持有一年的收益率是2%;

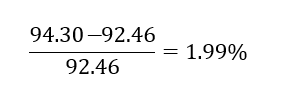

我们买一个2-year zero coupon bond,买入价是:92.46;

如果一年过去了,2-year bond还有maturity 1年,如果市场的spot rate如forward rate所预期,即当前的1-year spot rate是6.04%,那么此时我们卖出债券的价格是:94.30.

那么我们持有这个债券的收益率是:1.99%约等于2%,发现和持有1年期ZCB的收益率一模一样。

而在riding the yield curve要求了收益率曲线不变,那么在策略实施者眼里一年后的spot rate没有实现当初的forward rate,且比当初的forward rate更低,1年后的spot rate如下:

1-year是2%(低于当初市场预测6.04%),2-year是4%,3-year是7%,4-year是9%;

如果当初买的是1-year ZCB,此时到期,收益率为2%

如果当初买的是2-year ZCB,买入价时92.46;

那么此时的卖出价是:98.04

那么这个策略的收益是:6.03%

所以riding the yield curve成功的关键是,未来的spot rate没有实现当前forward rate的预测,反而比forward rate更低。我们要求的yield curve stable,就是未来spot rate比forward rate预测更低的一种情况。当然未来spot rate更低更好,例如1-year spot rate是0.2%,2-year是1%等等,比yield curve stable更低,做类似riding the yield curve策略更好。

而在buy and hold中,相当于passive的投资策略,是持有至到期,投资期是多长,就买入多长的债券hold到底,并不会在期间卖出;没有提前卖出就没有对卖出价格做出预期,所以收益率曲线是不是upward sloping都不影响。所以即便不是stable的yield curve,你也可以使用buy and hold;

我们是在stable yield curve的情况下,对比了riding the yield curve 比buy and hold更好。

corn0000 · 2018年06月08日

谢谢老师耐心讲解!棒棒哒🎉