NO.PZ2016012101000202

问题如下:

For a lessor, the leased asset appears on the balance sheet and continues to be depreciated when the lease is classified as:

选项:

A.a sales-type lease.

B.an operating lease.

C.a financing lease.

解释:

B is correct.

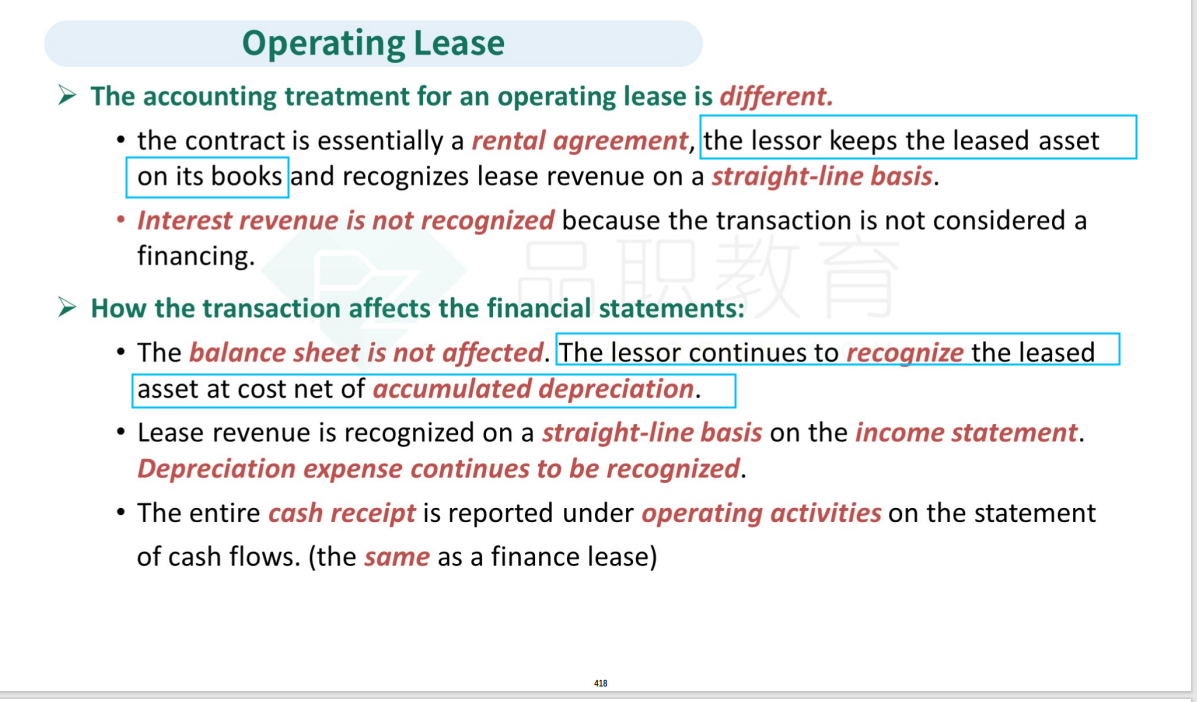

When a lease is classified as an operating lease, the underlying asset remains on the lessor’s balance sheet. The lessor will record a depreciation expense that reduces the asset’s value over time.

解析:对于出租人来说,租赁资产仍然确认在出租人账上且继续计提折旧费用。那么这种租赁模式属于下列哪种。

国际准则下,lessor角度的会计处理分为operating lease和finance lease两种:

(1)Operating lease:资产确认在lessor账上,lessor基于资产账面价值计提折旧费用(选项B入选),收到的lease payment作为income确认在损益表中。

(2)Finance lease:资产从lessor资产负债表上remove掉,同时资产增加lease asset。在损益表中确认revenue、COGS和profit,因为资产已经从lessor账上消掉,lessor不用确认折旧费用(选项C不入选),但是因为是融资性质的,lessor要在损益表中确认interest income。

美国准则下分为三种:

(1)Operating lease和国际准则operating lease会计处理相同。

(2)Finance lease:

- Sales-type lease和国际准则finance lease处理方法相同。(选项A不入选)

- Direct finance lease是资产从lessor资产负债表上remove掉,同时增加lease receivable,因为资产已经从lessor账上消掉,lessor不用确认折旧费用,但是因为是融资性质的,lessor要在损益表中确认interest income。与sales-type lease/国际准则finance lease的区别是,direct finance lease不确认selling profit。

老师,Lessor 这块,在讲Operating lease 的时候,说的The balance sheet is not affected. => 这个指的不是说B/S 不受影响吗?

为啥还是说有折旧呢?