NO.PZ201512020800000104

问题如下:

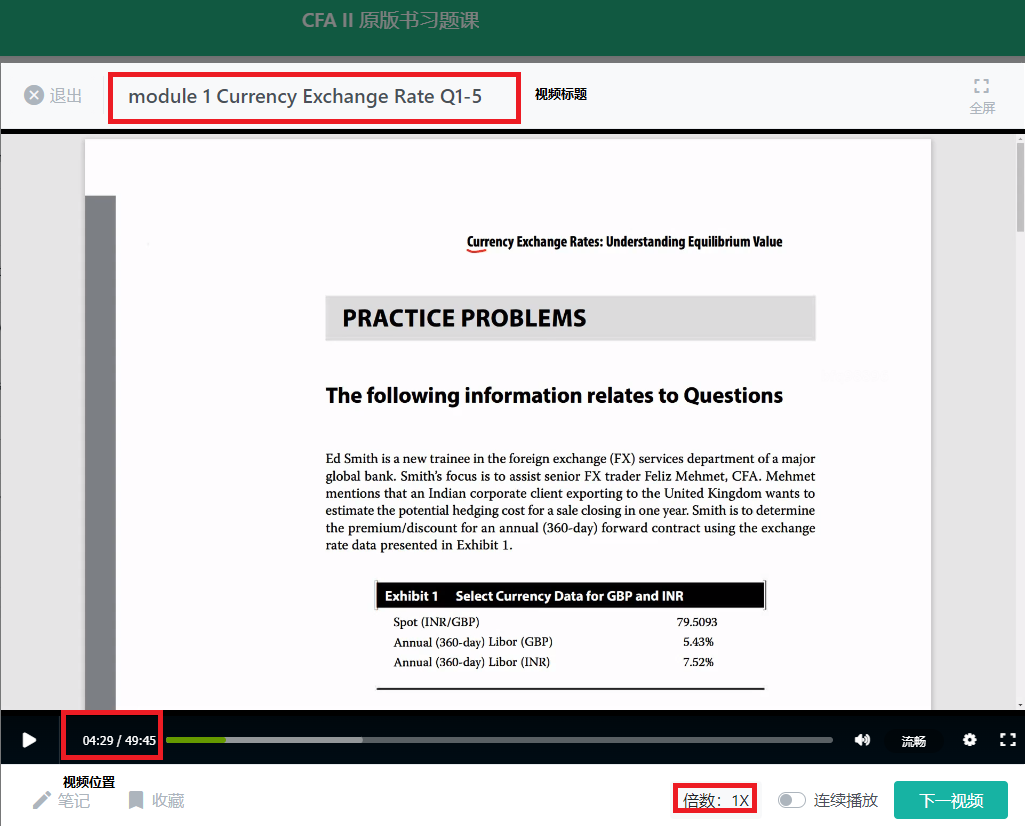

Ed Smith is a new trainee in the foreign exchange (FX) services department of a major global bank. Smith’s focus is to assist senior FX trader, Feliz Mehmet, CFA. Mehmet mentions that an Indian corporate client exporting to the United Kingdom wants to estimate the potential hedging cost for a sale closing in one year. Smith is to determine the premium/discount for an annual (360 day) forward contract using the exchange rate data presented in Exhibit 1.

Exhibit 1. Select Currency Data for GBP and INR

Mehmet is also looking at two possible trades to determine their profit potential. The first trade involves a possible triangular arbitrage trade using the Swiss, US and Brazilian currencies, to be executed based on a dealer’s bid/offer rate quote of 0.5161/0.5163 in CHF/BRL and the interbank spot rate quotes presented in Exhibit 2.

Exhibit 2. Interbank Market Quotes

Mehmet is also considering a carry trade involving the USD and the Euro. He anticipates it will generate a higher return than buying a one-year domestic note at the current market quote due to low US interest rates and his predictions of exchange rates in one year. To help Mehmet assess the carry trade, Mehmet provides Smith with selected current market data and his one year forecasts in Exhibit 3.

Exhibit 3. Spot Rates and Interest Rates for Proposed Carry Trade

Finally, Mehmet asks Smith to assist with a trade involving a US multinational customer operating in Europe and Japan. The customer is a very cost conscious industrial company with a AA credit rating and strives to execute its currency trades at the most favorable bid/offer spread. Because its Japanese subsidiary is about to close on a major European acquisition in three business days, the client wants to lock in a trade involving the Japanese yen and the Euro as early as possible the next morning, preferably by 8:05 AM New York time.

At lunch, Smith and other FX trainees discuss how best to analyze currency market volatility from ongoing financial crises. The group agrees that a theoretical explanation of exchange rate movements, such as the framework of the international parity conditions, should be applicable across all trading environments. They note such analysis should enable traders to anticipate future spot exchange rates. But they disagree on which parity condition best predicts exchange rates, voicing several different assessments. Smith concludes the discussion on parity conditions by stating to the trainees:

“I believe that in the current environment both covered and uncovered interest rate parity conditions are in effect.”

The conversation next shifts to exchange rate assessment tools, specifically the techniques of the IMF Consultative Group on Exchange Rate Issues (CGER). CGER uses a three-part approach including the Macroeconomic Balance Approach, the External Sustainability Approach, and a Reduced Form Econometric Model. Smith asks Trainee #1 to describe the three approaches. In response, Trainee #1 makes the following statements to the other trainees and Smith:

Statement 1 Macroeconomic Balance focuses on the stocks of outstanding assets and liabilities.

Statement 2 Reduced Form has a weakness in underestimating future appreciation of undervalued currencies.

Statement 3 External Sustainability centers on adjustments leading to long-term equilibrium in the capital account.

4. The factor least likely to lead to a narrow bid/offer spread for the industrial company’s needed currency trade is the:

选项:

A.timing of its trade.

B.company’s credit rating.

C.pair of currencies involved.

解释:

B is correct.

While credit ratings can affect spreads, the trade involves spot settlement, i.e. two business days after the trade date, so the spread quoted to this highly rated (AA) firm is not likely to be much tighter than the spread that would be quoted to a somewhat lower rated (but still high quality) firm. The relationship between the bank and client, the size of the trade, the time of day the trade is initiated, the currencies involved and the level of market volatility are likely to be more significant factors in determining the spread for this trade.

考点:factors that affect the bid/offer spread 其中的一个因素。

解析: 存在四个影响银行间市场间BID-ASK的SPREAD的因素,它们分别是交易币种、交易时间短、市场的波动性以及远期汇率间的SPREAD.

在本题中,日元和欧元是属于经常交易的货币,所以会降低SPREAD.

本题中交易时间在纽约时间6点到8点之间,这属于最大两个交易市场开市时间,所以也会降低SPREAD.

B选项不属于上述四个影响因素,公司信用好坏,通常不影响即期汇率的报价,所以本题中不予考虑。

请问这道大题完整版题目以及讲解在哪?我想练一下