NO.PZ2018062007000077

问题如下:

To determine the price of an option today, the binomial model requires:

选项:

A.

selling one put and buying one offsetting call.

B.

buying one unit of the underlying and selling one matching call.

C.

using the risk- free rate to determine the required number of units of the underlying.

解释:

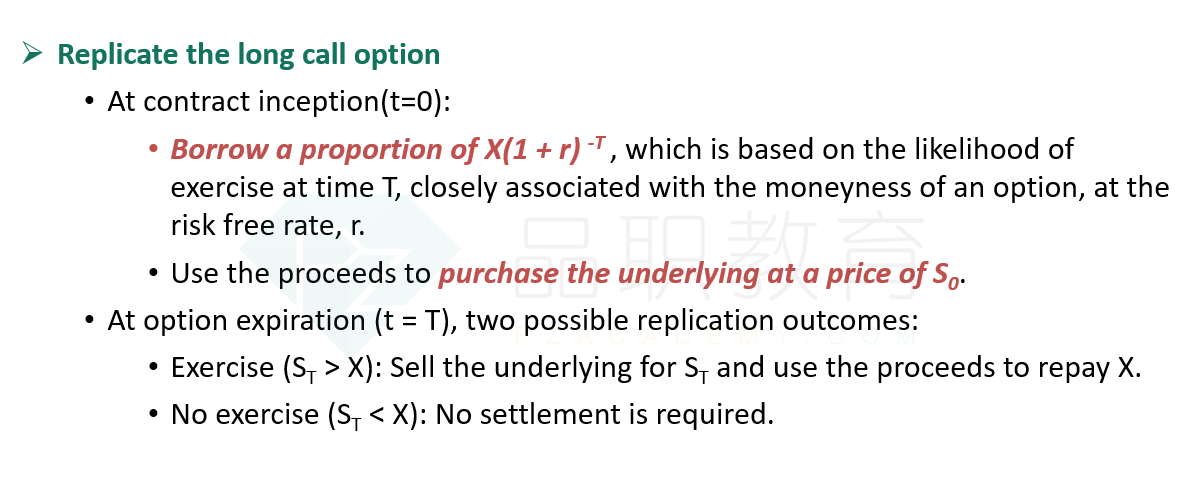

C is correct. Pricing an option relies on the facts that a perfectly hedged investment earns the risk- free rate and that, based on the binomial option pricing model, the size of the two possible changes in the option price (meaning the potential step up or step down in the option value) after one period are equivalent.

中文解析:

本题考察的是用hedged portfolio 的方法对二叉树进行定价。注意V0 =hS0 -c0, 其中short call=long stock - long rf ,因为我们可以用long stock与short call相结合,构建出无风险组合。那么也可以用无风险组合与stock相结合,构造出short call。

所以无论是long call 还是short call,都等于long stock +short rf 吗?