NO.PZ2023010301000065

问题如下:

All else being equal, the difference between the nominal spread and the Z-spread for a non-Treasury security will most likely be larger when the:

选项:

A.yield curve is steep.

yield curve is flat.

security has a bullet maturity rather than an amortizing structure.

解释:

Correct Answer: A

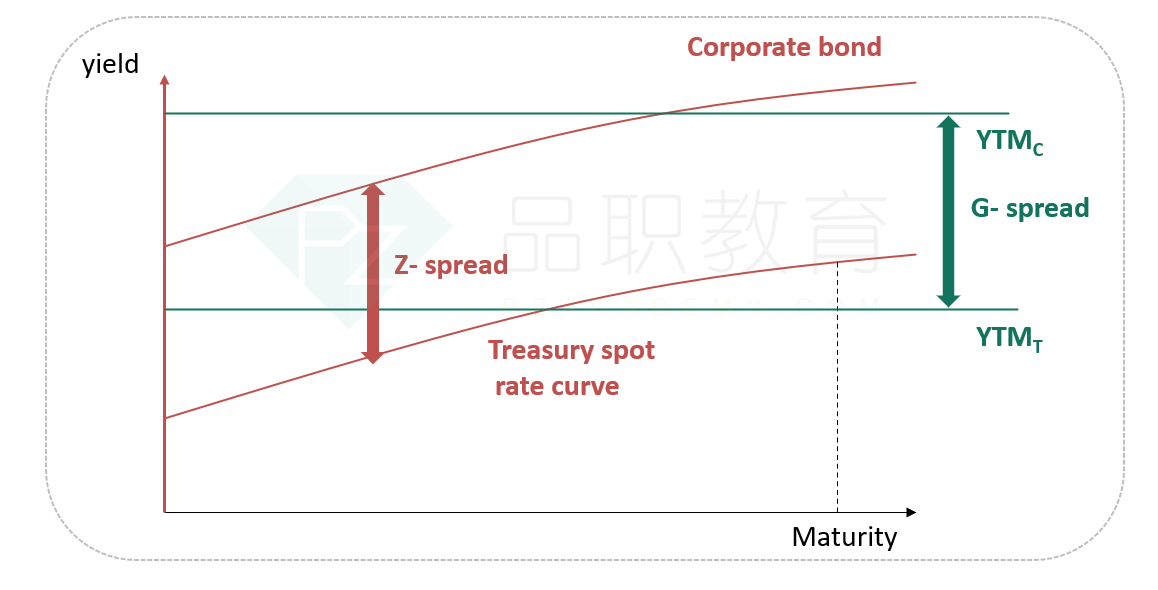

The main factor causing any difference between the nominal spread and the Z-spread is the shape of the Treasury spot rate curve. The steeper the spot rate curve, the greater the difference.

可以用图来解释一下这题吗?这几个概念不是很明白。