NO.PZ2023010301000059

问题如下:

Which of the following statements describing a par curve is incorrect?

选项:

A.A par curve is obtained from a spot curve.

All bonds on a par curve are assumed to have different credit risk.

A par curve is a sequence of yields-to-maturity such that each bond is priced at par value.

解释:

Correct Answer: B

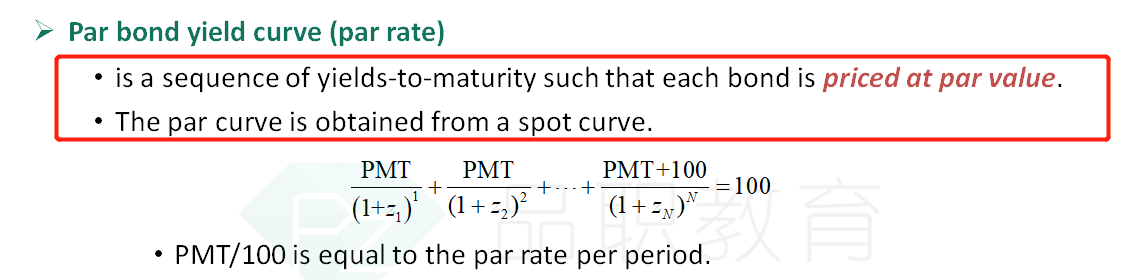

All bonds on a par

curve are assumed to have similar, not different, credit risk. Par curves are

obtained from spot curves and all bonds used to derive the par curve are

assumed to have the same credit risk, as well as the same periodicity,

currency, liquidity, tax status, and annual yields. A par curve is a sequence

of yields-to-maturity such that each bond is priced at par value.

A选项为什么是对的呢?