NO.PZ202304050100007601

问题如下:

(1) After translating Consol-Can’s inventory and long-term debt into the parent company’s currency (US$), the amounts reported on Consolidated Motor’s financial statements on 31 December 20X2 would be closest to (in millions):

选项:

A.$71 for inventory and $161 for long-term debt.

$71 for inventory and $166 for long-term debt.

$73 for inventory and $166 for long-term debt.

解释:

When the parent company’s currency is used as the functional currency, the temporal method must be used to translate the subsidiary’s accounts. Under the temporal method, monetary assets and liabilities (e.g., debt) are translated at the current (year-end) rate, nonmonetary assets and liabilities measured at historical cost (e.g., inventory) are translated at historical exchange rates, and non-monetary assets and liabilities measured at current value are translated at the exchange rate at the date when the current value was determined. Because beginning inventory was sold first and sales and purchases were evenly acquired, the average rate is most appropriate for translating inventory and C$77 million × 0.92 = $71 million. Long-term debt is translated at the year-end rate of 0.95. C$175 million × 0.95 = $166 million.

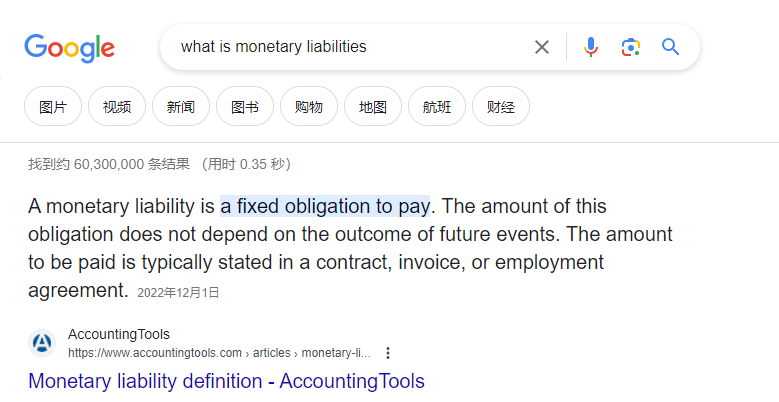

Why is LT debt considered a monetary liability?

Isn't long-term debt a non-monetary liability?