NO.PZ2016031201000044

问题如下:

A European put option on a dividend-paying stock is most likely to increase if there is an increase in:

选项:

A.carrying costs.

B.the risk-free rate.

C.dividend payments.

解释:

C is correct.

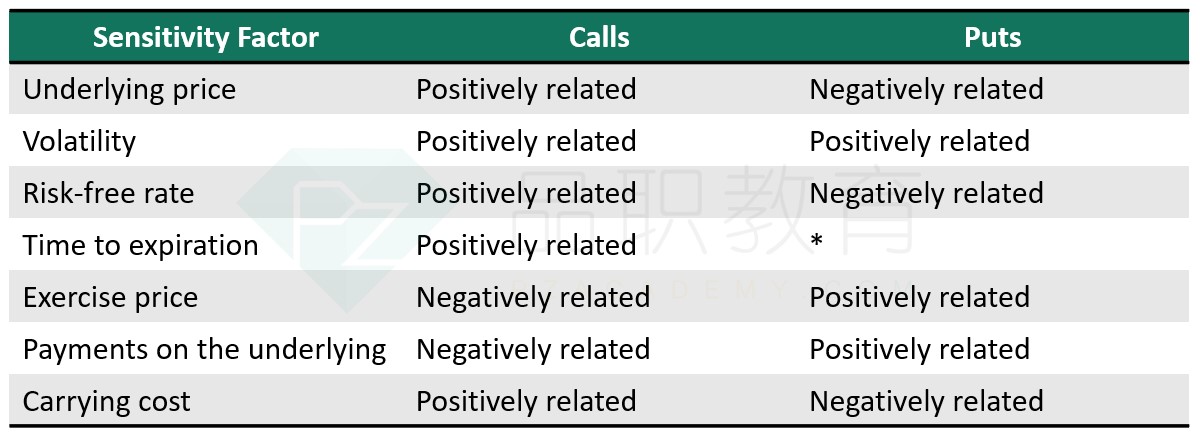

Payments, such as dividends, reduce the value of the underlying which increases the value of a European put option. Carrying costs reduce the value of a European put option. An increase in the risk-free interest rate may decrease the value of a European put option.

中文解析:

对于欧式看跌期权,因为只能到期行权,他在t时刻的value就是Max[0, X/(1 + r)T -St],如果股票分红增加,分红派息会导致股票的每股净资产减少,所以股价必然下跌。另外由于股票分红时一般会进行除权处理,导致股价降低。那么St就会减小,从而期权的value会增加。

另外,从公式可以看出,无风险利率上升,分母变大,会导致期权价值减少。

持有成本增加,会导致标的资产价格上升,即St增加,所以会减少看跌期权的价值

如题