NO.PZ2023010903000072

问题如下:

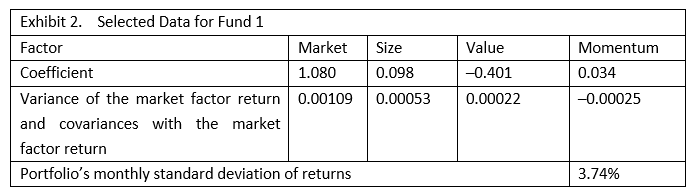

Based on Exhibit 2, the portion of total portfolio risk that is explained by the market factor in Fund 1’s existing portfolio is closest to:

选项:

A.3%

81%

87%

解释:

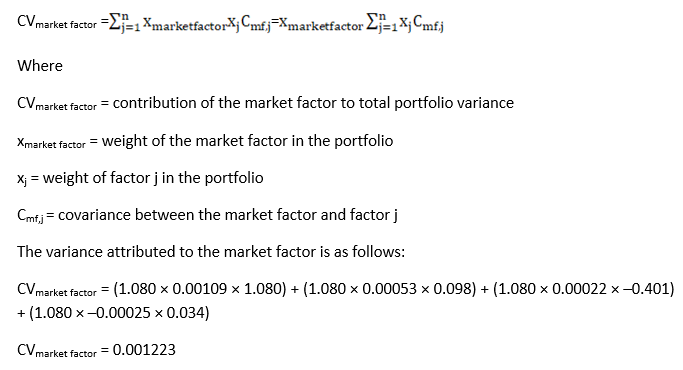

The portion of total portfolio risk explained by the market factor is calculated in two steps. The first step is to calculate the contribution of the market factor to total portfolio variance as follows:

The second step is to divide the resulting variance attributed to the market factor by the portfolio variance of returns, which is the square of the standard deviation of returns:

Portion of total portfolio risk explained by the market factor = 0.001223/(0.0374)2

Portion of total portfolio risk explained by the market factor = 87%

为什么计算market 和其他因子的影响的时候不用乘2呢,按照用画图(类似九宫格)的方法来求组合的方差的时候,是要乘2呀,比如2*w1*w2*covariance