NO.PZ202112010200000106

问题如下:

The portfolio alternative with the least exposure to convexity is the:

选项:

A.bullet

portfolio.

barbell portfolio

equally weighted portfolio.

解释:

A is correct.

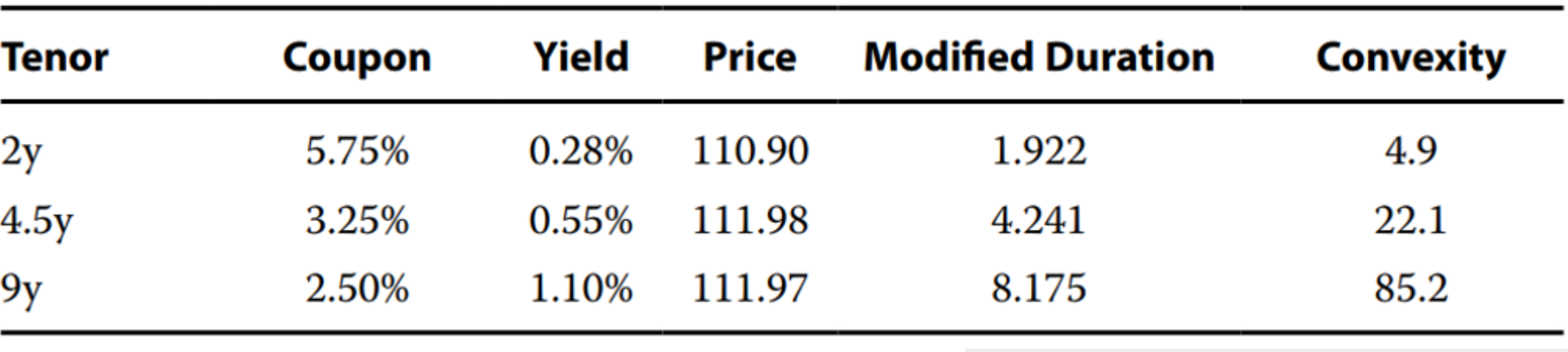

The bullet portfolio has the same convexity as the 45.5-year bond, or 22.1. The barbell portfolio in B has portfolio convexity of 45.05, = (4.9 + 85.2)/2, while the equally weighted portfolio has portfolio convexity of 37.4, = (4.9 + 22.1 + 85.2)/3

请问这句话是什么意思?“The bullet portfolio has the same convexity as the 45.5-year bond, or 22.1”。bullet由2年期债券构成,convexity应该是4.9吧?