NO.PZ202206140600000403

问题如下:

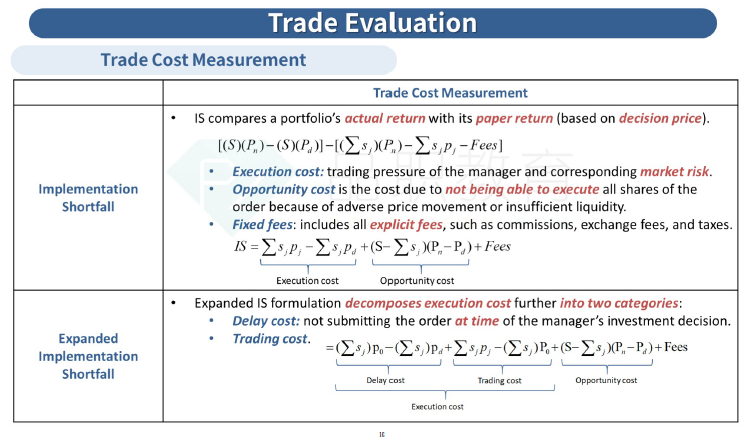

Based on Exhibit 1, the component of the expanded implementation shortfall for the trading of the securities from the UPX Fund that is most favorable to Quagmire Funds is the:选项:

A.delay cost. B.trading cost. C.opportunity cost.解释:

SolutionB is correct. Expanded implementation shortfall (IS) = Delay cost + Trading cost + Opportunity cost + Fees. Note that to reflect that shares are being sold rather than purchased, the “number of shares sold” is a negative value.

Delay cost = (Number of shares sold × Arrival price) – (Number of shares sold × Decision price)

= Value of shares sold at arrival price – Value of shares sold decision price

Delay cost = (–$5,175,800) – (–$5,124,300) = –$51,500,

which reduces the expanded IS.

Trading cost = (Total shares sold × Execution price) – (Number of shares sold × Arrival price)

= Value of shares sold at execution price – Value of shares sold at arrival price

Trading cost = (–$5,545,600) – (–$5,175,800) = –$369,800,

which reduces the expanded IS.

Opportunity cost: Based on not selling the desired number of shares. All shares were sold, which makes this value zero.The trading cost component is the most favorable to Quagmire Funds because it reduces the expanded IS the most.

A is incorrect. The delay cost component has less impact on the expanded IS than the trade cost component.

C is incorrect. Because all the shares were sold, the opportunity cost is zero. The delay cost and trading cost components both reduced the expanded IS.

我看同学提到正负有点迷惑,可以理解为Decision price