NO.PZ2023040502000017

问题如下:

You

are a junior analyst at an asset management firm. Your supervisor asks you to analyze

the return drivers for one of the firm’s portfolios.

Model 3: RETi = b0 + bMRKTMRKTi

+ bHMLHMLi + bVIXVIXi + bSMBSMBi

+ bMOMMOMi + εi.

Your supervisor is concerned about conditional

heteroskedasticity in Model 3 and asks you to perform the Breusch–Pagan (BP)

test. At a 5% confidence level, the BP critical value is 11.07. You run the

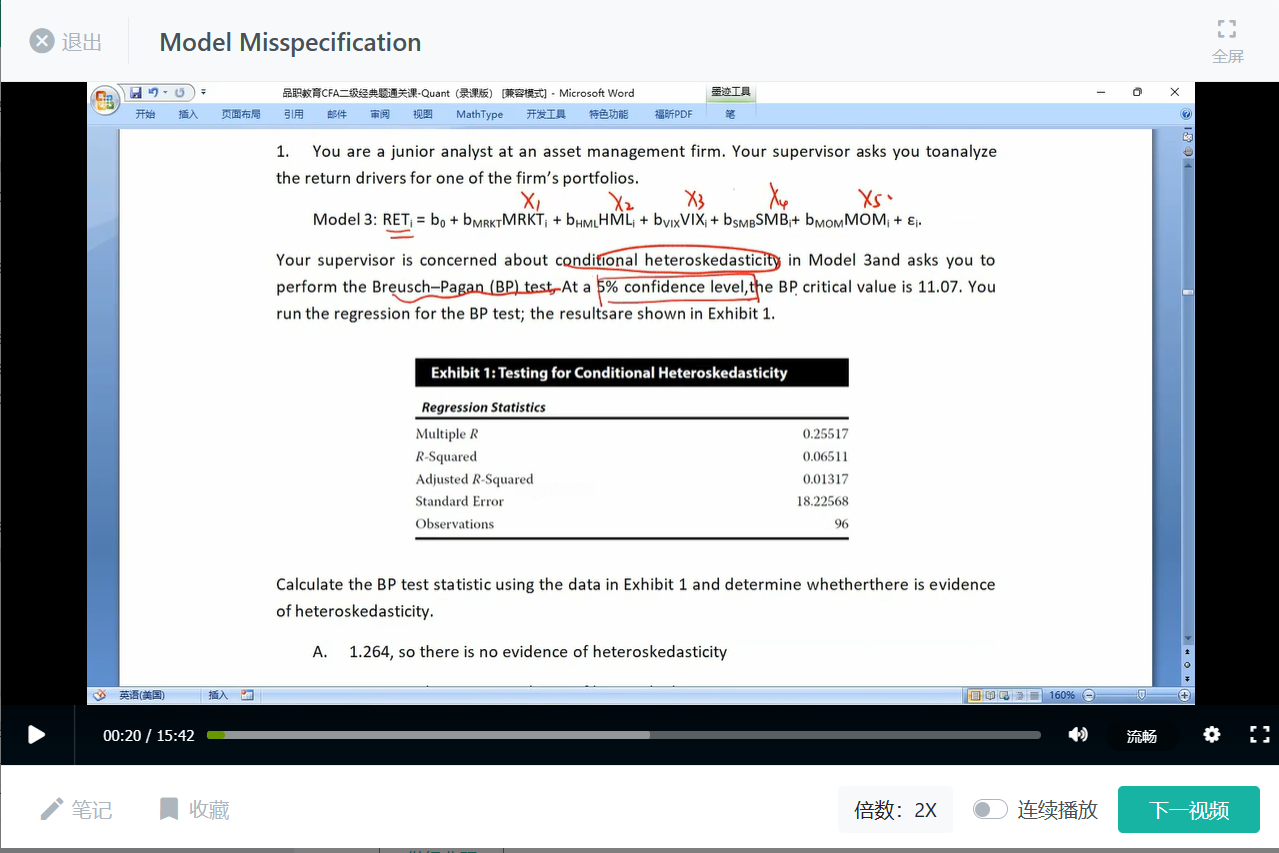

regression for the BP test; the results are shown in Exhibit 1.

Calculate the BP test statistic using the data in Exhibit

1 and determine whether there is evidence of heteroskedasticity.

选项:

A.1.264, so there is no evidence of heteroskedasticity

6.251, so there is no evidence of heteroskedasticity

81.792, so there is evidence of heteroskedasticity

解释:

B is correct. The BP test statistic is calculated as

nR2, where n is the number of observations and R2 is from

the regression for the BP test. So, the BP test statistic= 96 × 0.06511 =

6.251. This is less than the critical value of 11.07, so we cannot reject the

null hypothesis of no heteroskedasticity. Thus, there is no evidence of heteroskedasticity.

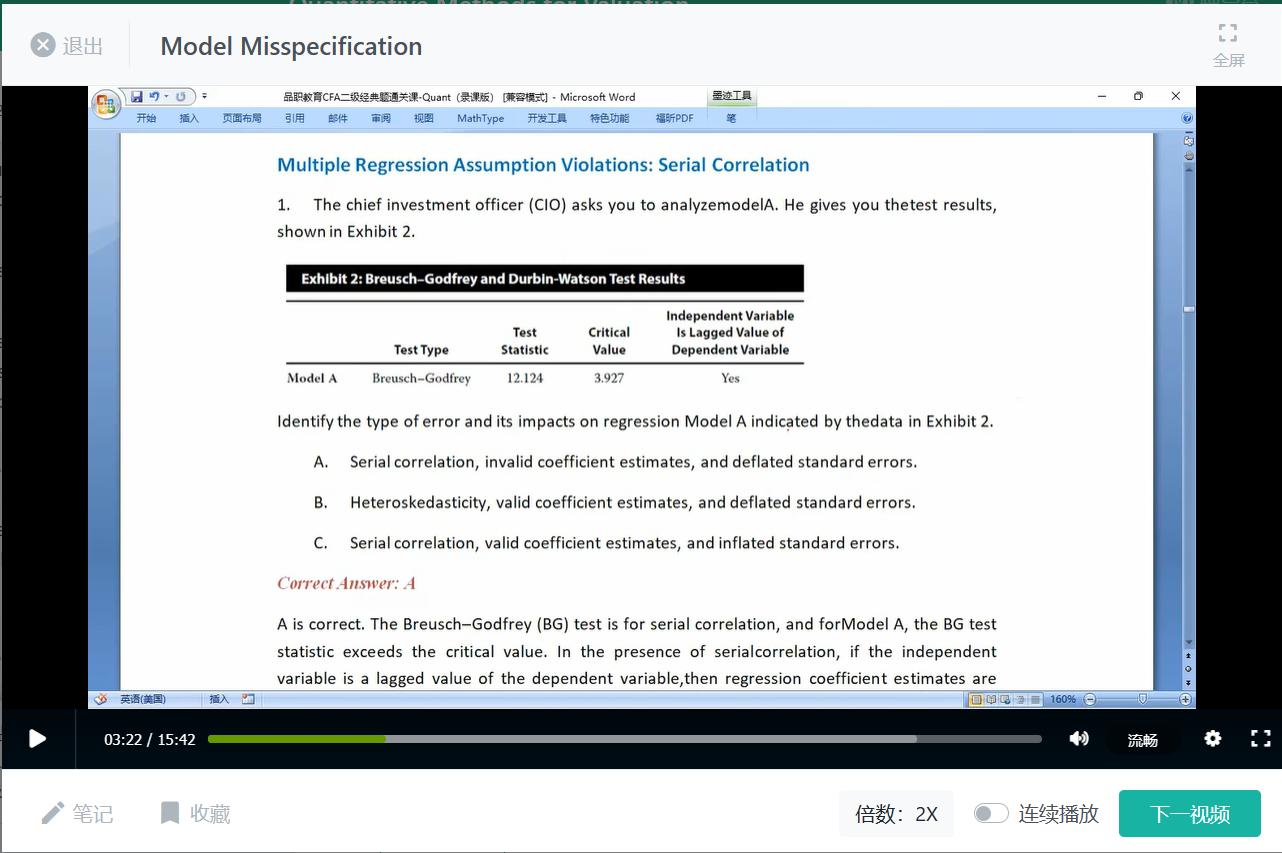

助教你好。我发现几个module的经典题讲解差两个部分,分别是: multiple regression assumption violation: heteroskedasticity 和 multiple regression assumption violation: serial correlation