NO.PZ2023041003000030

问题如下:

Statement #3

“Using put–call parity,

you can also create synthetic options on forward contracts. The data in Exhibit

1 can be used to establish the price of such a synthetic put.”

The price of the

synthetic put in Statement #3 is closest to:

选项:

A.$15.48.

$16.33.

$18.00.

解释:

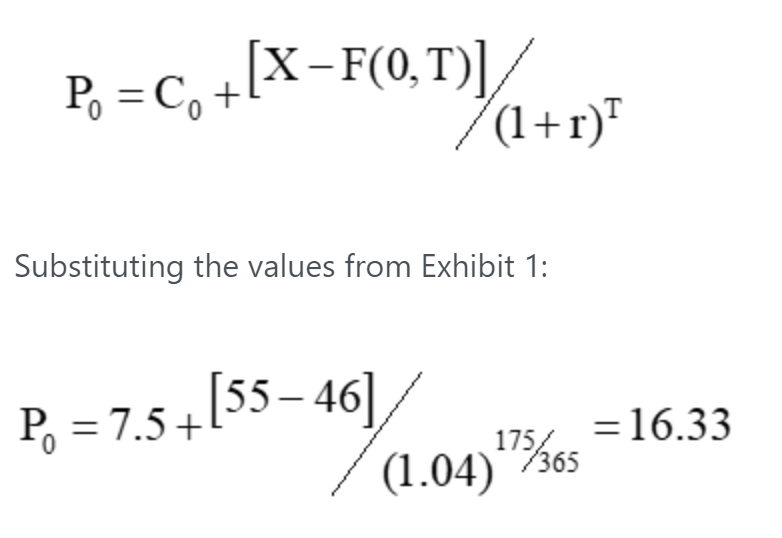

When dealing with

forward contracts, as in Burke’s Statement #3, put–call parity must be

modified. Rather than shorting the stock, a forward contract is used. The

current stock price, S

Substituting the

values from Exhibit 1:

老师,您好!

如下图

公式中的X应该是指债券的价格吧,为什么是用行权价格55来替换呢?这是call的行权价还是put的行权价?麻烦补充一下,谢谢!