NO.PZ2019052001000131

问题如下:

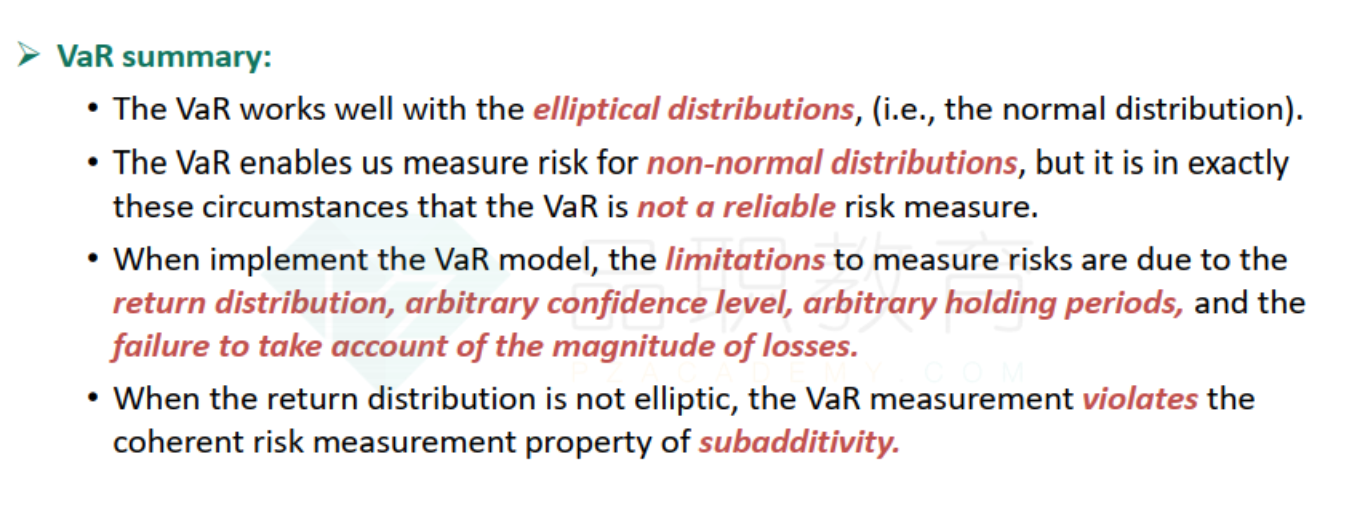

Which of the following statement about VaR estimates is correct?

选项:

A.

Before comparing the VaR estimates, it is important to make sure that they are expressed in the same confidence intervals and time horizons.

B.

Once expressed in the same confidence intervals and time horizons, VaR estimates is free from variability and inconsistency.

C.

The VaR estimate of two portfolios is equal to the sum of these two individual portfolios.

D.

All of above.

解释:

A is correct.

考点:defining risk measures

解析:在相同的置信区间和时间范围下,VaR仍可能受到其它因素影响,例如所选时间序列不同、计算均值和方差的方法不同、模拟数不同(例如使用蒙特卡洛模拟的数据量)等等,所以B选项错。C选项,描述的性质是subadditivity,但是VaR不具备这样的性质,因为两个portfolio组合后的VaR小于各自计算出的VaR之和。

B选项不明白什么意思。