NO.PZ2023041102000006

问题如下:

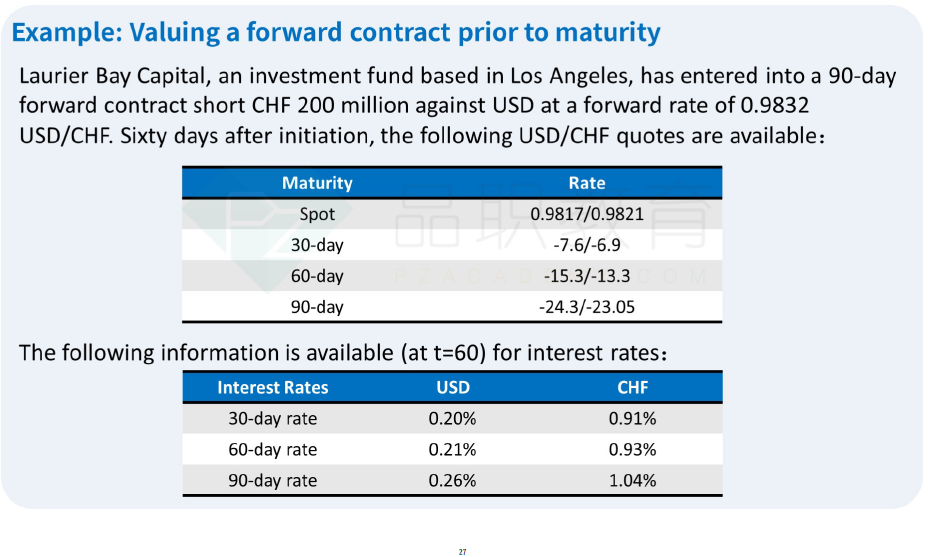

Anna Goldsworthy is the chief financial officer of a manufacturing firm headquartered in the United Kingdom. Goldsworthy gathers the exchange rates from Dealer A in Exhibit 1.

In three months, the firm will receive EUR 5,000,000 (euros) from another customer. Six months ago, the firm sold EUR 5,000,000 against the GBP using a nine-month forward contract at an all-in price of GBP/EUR 0.7400. To mark the position to market, Underwood collects the GBP/EUR forward rates in Exhibit 2.

Based on Exhibits 1, 2, the mark-to-market gain for Goldsworthy’s forward position is closest to:

选项:

A.GBP 20,470. B.GBP 20,500. C.GBP 21,968.解释:

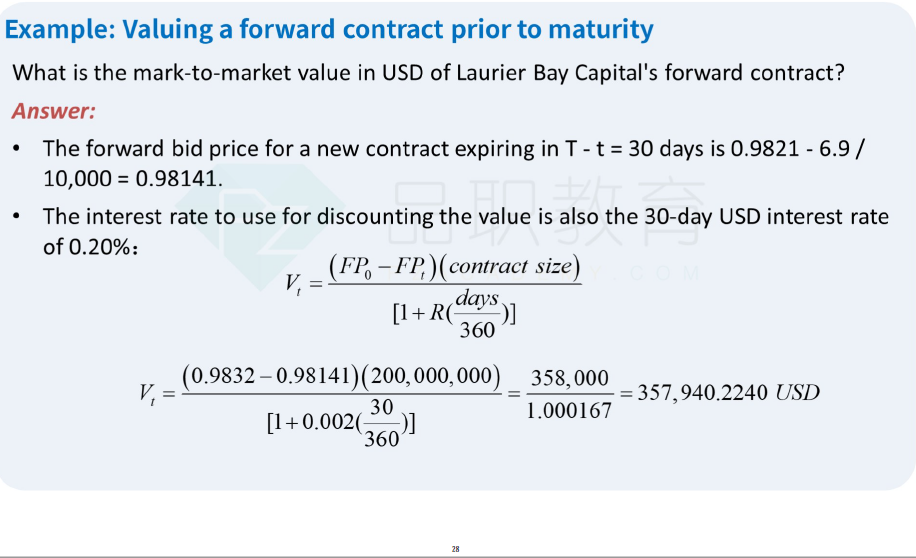

Marking her nine-month contract to market six months later requires buying GBP/EUR three months forward. The GBP/EUR spot rate is 0.7342/0.7344, and the three-month forward points are 14.0/15.0. The three-month forward rate to use is 0.7344 + (15/10000) = 0.7359. Goldsworthy sold EUR 5,000,000 at 0.7400 and bought at 0.7359. The net cash flow at the settlement date will equal EUR 5,000,000 × (0.7400 – 0.7359) GBP/EUR = GBP 20,500. This cash flow will occur in three months, so we discount at the three-month GBP Libor rate of 58 bps:

(1)6个月前,公司签订远期合约,约定9个月后以f0的价格卖出EUR,支付GBP,把EUR当做base currency/苹果来考虑,f0价格是0.74 GBP/EUR;

(2)现在,盯市价值为远期与spot汇率的差,对于short 方,即期汇率越降低,合约越值钱;相当于以市场汇率重新卖出一份3个月的远期EUR,再平仓之前9个月的合约。

(3)从dealer角度看,是现在要买入远期EUR,卖GBP,卖什么就把什么当做base currency/苹果来考虑,所以这个时候报价形式要转化为(1/0.7344~1/0.7342)EUR/GBP,把GBP当成苹果,要以便宜的价格买苹果,所以价格取了倒数的倒数0.7344。

另外这样思考过程好长,是否有正确的或者简化的思路?