NO.PZ2022122801000036

问题如下:

Zoe reviews the asset

allocation in Exhibit 3, derived from a mean–variance optimization (MVO) model

.

The risk free rate is 2%. Determine if the asset allocation achieves optimal Sharpe ratio. Justify your response.

选项:

解释:

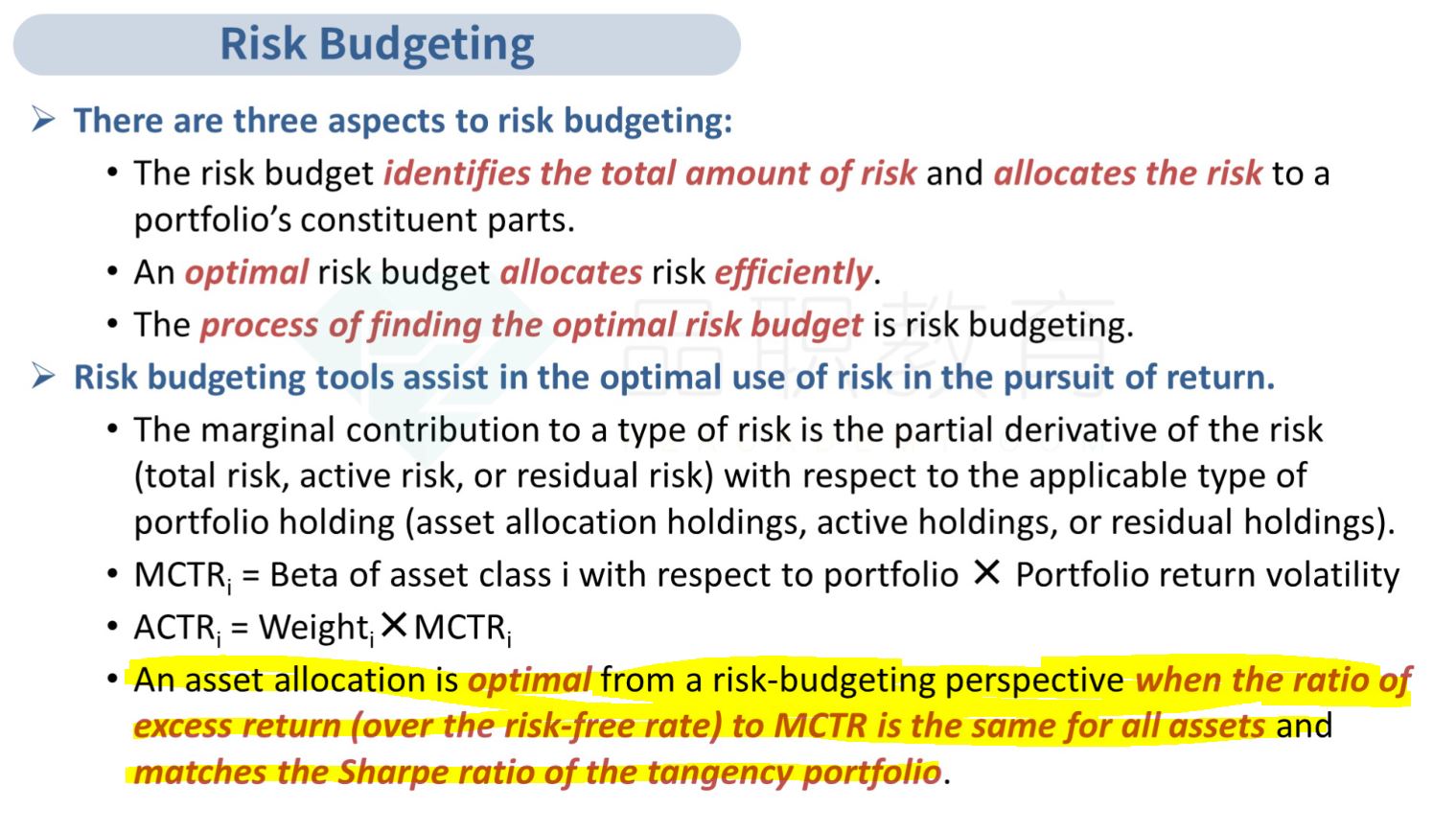

An asset allocation is optimal from a risk-budgeting perspective when the ratio of excess return (over the risk-free rate) to MCTR is the same for all assets and matches the Sharpe ratio of the tangency portfolio.

Since the Excess Return/MCTR is the same for all asset class, the asset allocation is optimal from a risk-budgeting perspective and achieves optimal Sharpe ratio.

如题