上面题目这么答题得分么?有需要提升的么?

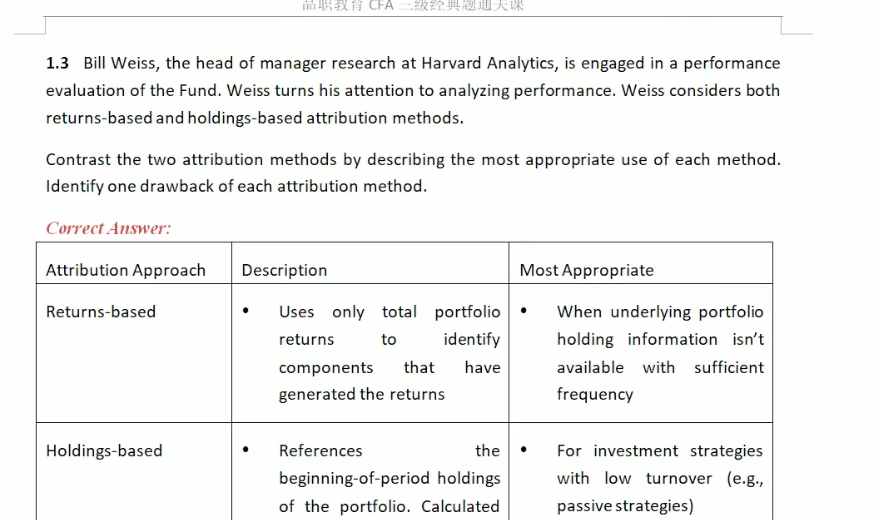

returns-based attribution uses only the total portfolio returns. It is appropriate when the underlying portfolio holding information is not available. However, it is least accurate and is most vulnerable to data manipulation.

Holding-based attribution uses the beginning holdings of the portfolio It is appropriate for investment strategies with little turnover. However, it fails to capture the impact of any transactions.