NO.PZ2023032703000058

问题如下:

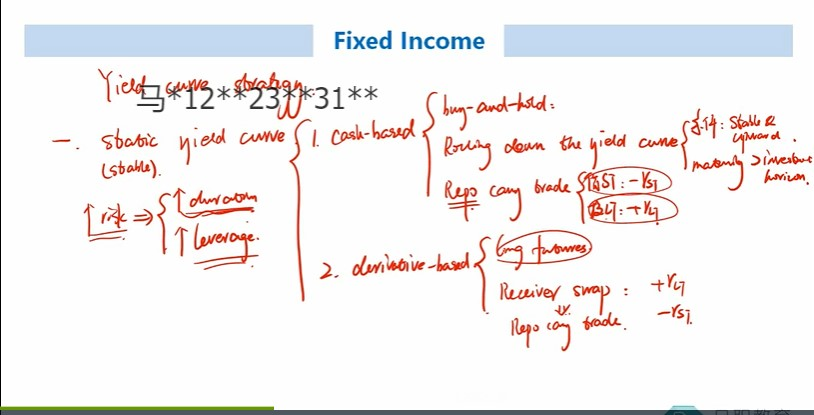

An analyst manages an active fixed-income fund that is benchmarked to the Bloomberg Barclays US Treasury Index. This index of US government bonds currently has a modified portfolio duration of 7.25 and an average maturity of 8.5 years. The yield curve is upward-sloping and expected to remain unchanged. Which of the following is the least attractive portfolio positioning strategy in a static curve environment?

选项:

A.

Purchasing a 10-year zero-coupon bond with a yield of 2% and a price of 82.035

B.

Entering a pay-fixed, 30-year USD interest rate swap

C.

Purchasing a 20-year Treasury and financing it in the repo market

解释:

B is correct. The 30-year pay-fixed swap is a short duration position and also results in negative carry (that is, the fixed rate paid would exceed MRR received) in an upward-sloping yield curve environment; therefore, it is the least attractive static curve strategy. In the case of a.), the manager enters a “buy-and- hold” strategy by purchasing the 10-year zero-coupon bond and extends duration, which is equal to 9.80 = 10/1.02 since the Macaulay duration of a zero equals its maturity, and ModDur = MacDur/(1+r) versus 7.25 for the index. Under c.), the manager introduces leverage by purchasing a long-term bond and financing it at a lower short-term repo rate.

这题麻烦给解释一下吧