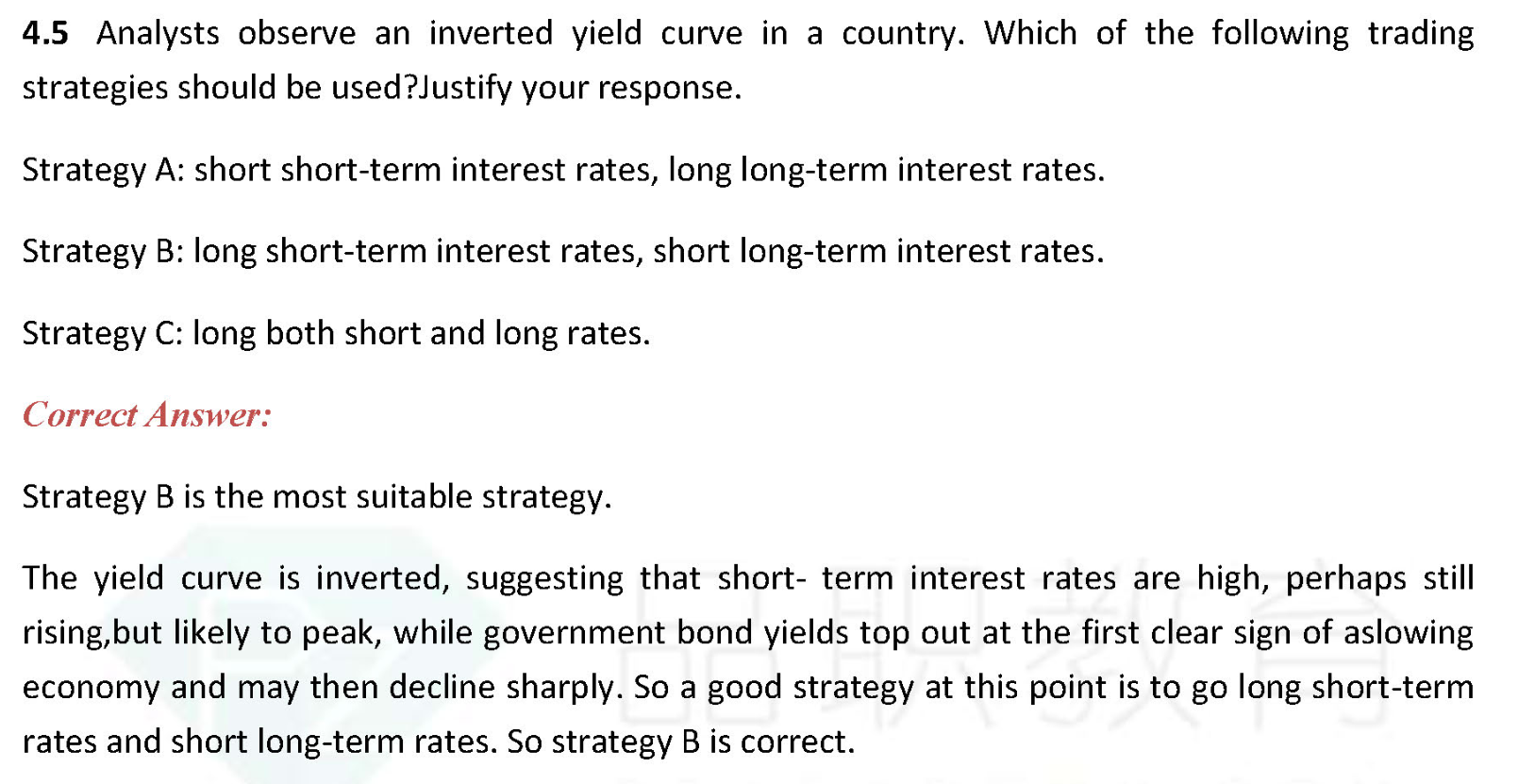

这里 short-term interest rate 是不是应该是指短期的固收产品?

结合到实务我的解题思路是:短期利率高,长期利率低(slowndown phase),即将会进入contraction (yield curve steepen)->ST interest rate is to fall and LT rate is to rise. 所以应该Long ST bond (锁定high yield 并且后面利率下降可以获得price appreciation) and Short LT bond (未来长期收益率上行,长久期债价格会下跌).

这个思路是否正确?请老师帮忙指正,谢谢!