NO.PZ202304050100007604

问题如下:

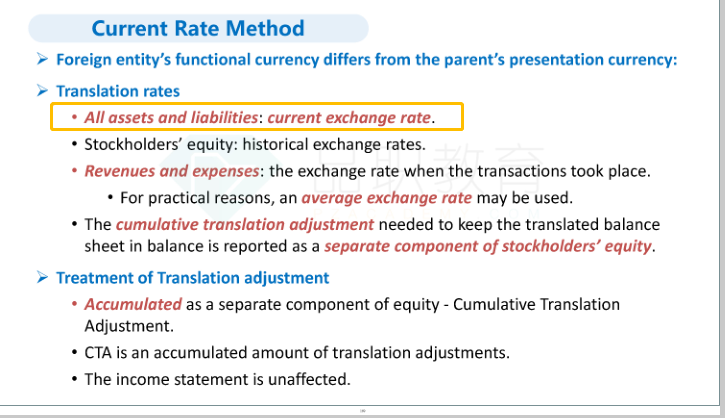

(4) What would be the balance sheet exposure to translation effects if the functional currency were changed? In response to the question, the balance sheet exposure (in C$ millions) would be closest to:

选项:

A.–19.

148.

400.

解释:

If the functional currency were changed, then Consol-Can would use the current rate method and the balance sheet exposure would be equal to net assets (total assets – total liabilities). In this case, 400 – 77 – 175 = 148.

老师,您好!

current rate method方法下的汇率风险敞口,解析说的是净资产(equity)部分,这部分应该是基于历史汇率转换吧,历史汇率是确定的,也就没有不确定性的风险了。

我理解应该是monetary的资产减去monetary负债,即monetary的净资产才会面临当前汇率的不确定性,应该是135+98-77-175 = -19,是吗?谢谢!