NO.PZ2015121802000052

问题如下:

Which of the following statement is most accurate about beta?

选项:

A.Beta is best described as the slope of the security market line.

B.Beta is best described as correlation of returns with those of the market portfolio.

C.Beta is best described as sensitivity of an asset's return to the return on market index.

解释:

C is correct.

A stock's beta is sensitivity of an asset's return to the return on market index.

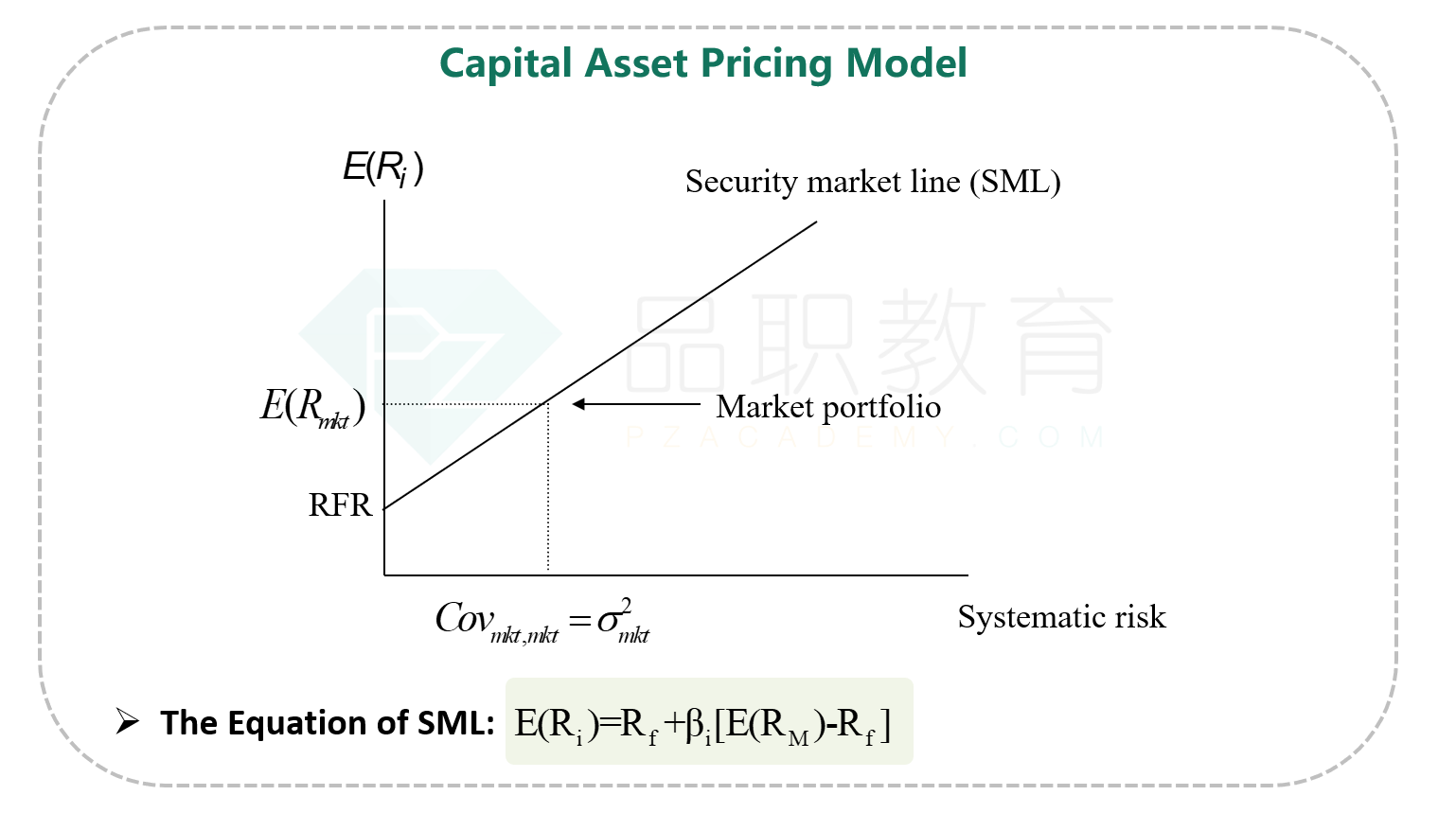

beta是SML线的斜率,market risk premium是SML线的横轴