CFA level II 课后题 Ryan Parisi Case 求full price of the treasury bond 为什么Coupon 用的FV (3,508)而不是PV (3,491)

Ryan Parisi Case Scenario

Ryan Parisi is a managing director in the derivatives group at High Ridge Partners, an investment management firm. Parisi specializes in advising institutional clients on the use of forward contracts in their portfolio management strategies. Parisi is preparing a response to questions from one of the firm’s US-based clients: Leslie Sheroda. Todd Curry, an intern in the derivatives group, will assist Parisi.

Leslie Sheroda oversees both equity and fixed-income portfolios for a pension fund. One month (30 days) ago, Sheroda had indicated that the pension fund expected a large inflow of cash in 60 days. In order to hedge against a potential rise in equity values over this period, Parisi advised Sheroda to enter into a long forward contract on the UAX 300 Index expiring in 60 days. Sheroda determined she was also underweight in one individual stock. Sixty days ago, she entered a long forward position on CHJ common stock, which does not pay a dividend. Sheroda has asked Parisi to calculate the value of her two forward positions today—that is, 30 days after the contracts were initiated. Parisi has collected the information in Exhibit 1 to carry out the valuation assignment.

Prior to the meeting, Parisi shows the spot price of the UAX 300 index in Exhibit 1 to Curry and asks how the 30-day forward price will relate to the current level of the index. Curry compares the spot index to the forward price.

Parisi asks Curry a second question: “Are you clear about how the value of a forward contract can change?” Curry responds, “Yes, I am. In general, the value of a forward contract may be positive or negative at the inception of the contract, during its life, and at the expiration of the contract.”

Using Exhibit 1, Parisi and Curry compute the value of the two forward contracts. Parisi continues the discussion about forward prices and asks, “Is it true that the forward price on an asset must equal the spot price of the asset on the expiration date of the forward contract? Explain why or why not.”

Curry responds, “At expiration, forward prices and spot prices must converge. If the spot price exceeds the forward price, then an investor could purchase the forward contract and execute the contract to purchase the underlying at the lower forward price and sell at the higher spot price and make an arbitrage profit. If the spot price is less than the forward price at expiration, then an investor could purchase the asset at the spot price and enter into a short forward contract to sell at the higher price, thus locking in a profit.”

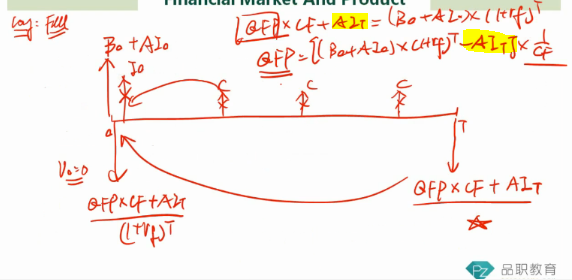

They move to valuation of a bond futures contract employed by Sheroda. Parisi provides Curry with the following information for a Treasury bond and calculates the price of a futures contract on this bond. The bond has a face value of $100,000, pays a 7% semiannual coupon, and matures in 15 years. The bond is priced at $156,000, has no accrued interest, and yields 2.5%. The futures contract expires in 8 months, and the annualized risk-free rate is 1.5%. There are multiple deliverable bonds, and the conversion factor for this bond is 1.098.