NO.PZ2016031202000028

问题如下:

The at-the-money European call option has one month remaining until expiration, the market value of the option is most likely:

选项:

A.

less than zero

B.

equal to zero

C.

greater than zero

解释:

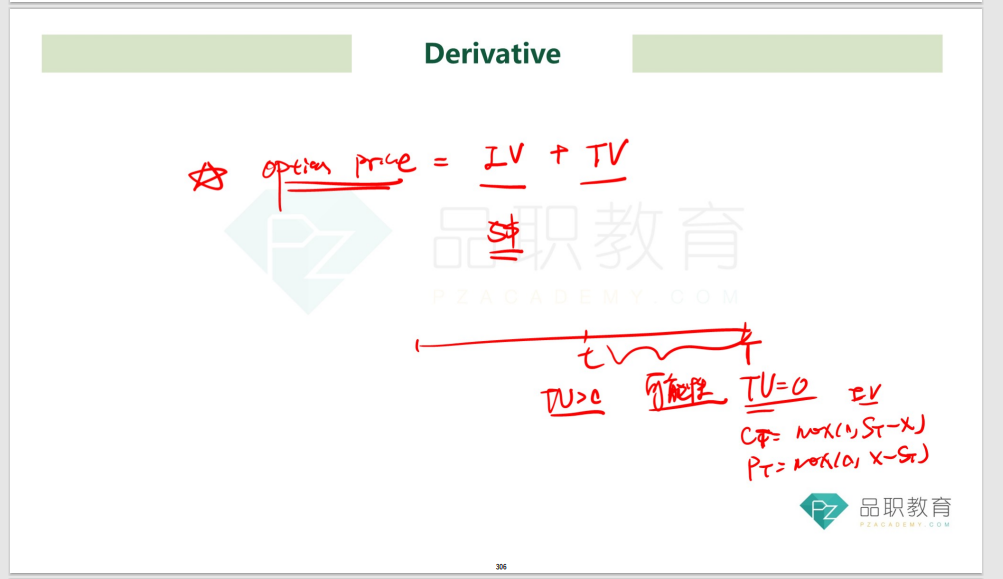

C is correct. The exercise value of at-the-money option is zero, but market value is greater than zero because of time value.

中文解析:

at the money的期权其内在价值为0,由于期权的价值等于内在价值+时间价值,内在价值为0,而期权还有1个月到期,意味着时间价值大于0,所以期权价值就是大于0的

rt……………………………………