NO.PZ2020011303000101

问题如下:

If the hazard rate is 1.5% per year for the first three years and 2.5% per year for the next three years, what is the probability of default during the first two years? What is the average hazard rate for the first five years? What is the probability of default between years two and five?

解释:

The probability of default during the first two years is 1-exp(−0.015 × 2) = 0.02955. The average hazardrate during the first five years is (1.5 × 3 + 2.5 × 2)/5 = 1.9%. The probability of default during the first five years is 1-exp(−0.019 × 5) = 0.09063. The probability of default between years two and five is 0.09063 − 0.02955 = 0.06107.

题目问:如果前三年的hazard rate为每年 1.5%,后三年为每年 2.5%,那么前两年的违约概率是多少?前五年的平均hazard rate是多少?第二年和第五年之间违约的概率是多少?

PD(0-2)=1-e^(-h*t)=1-e^(-1.5%*2)=0.02955

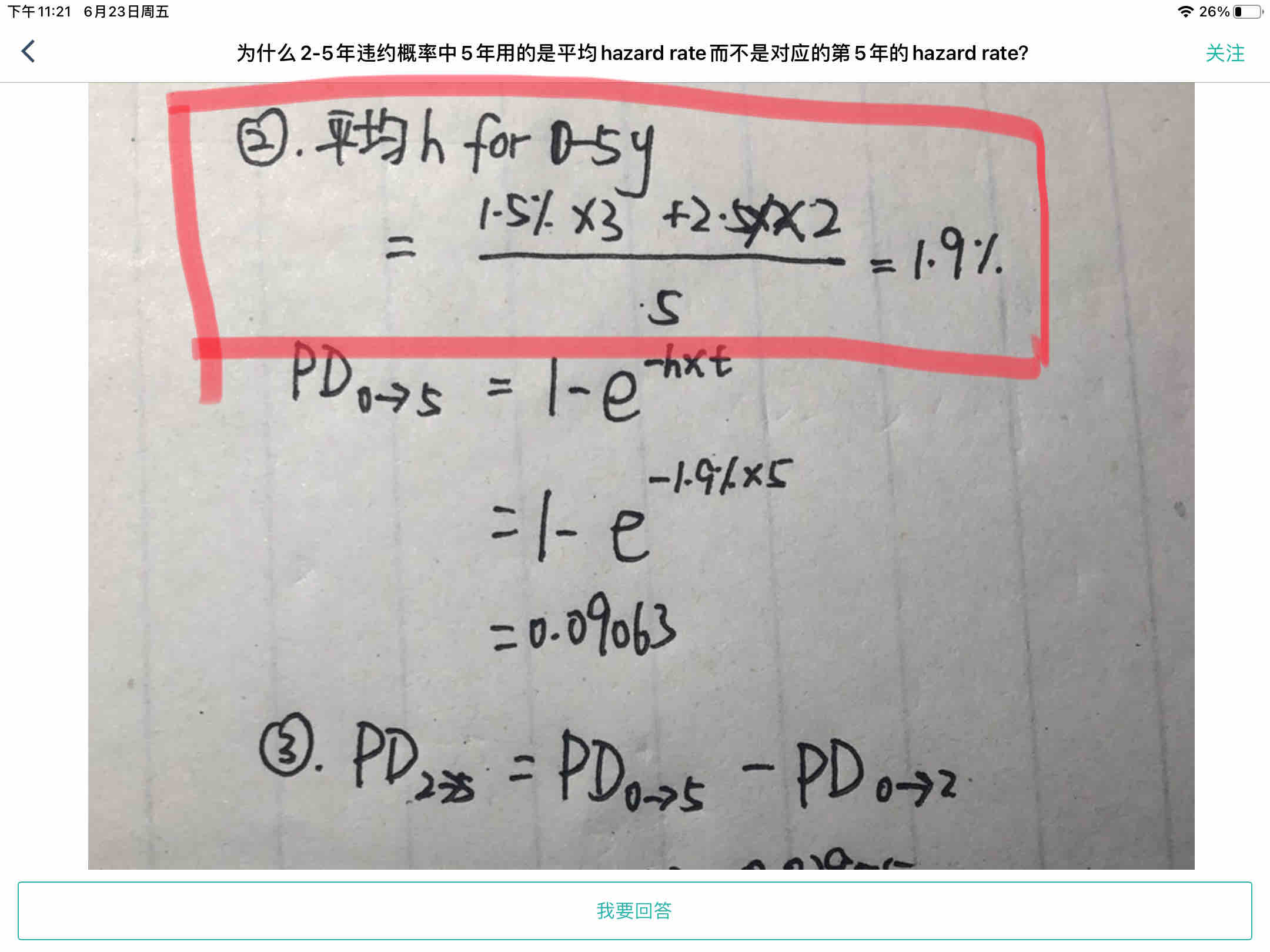

平均h for 0-5 year=(1.5%*3+2.5%*2)/5=1.9%

PD(0-5)=1-e^(-1.9%*5)=0.09063

PD(2-5)=PD(0-5) - PD(0-2)=0.09063-0.02955=0.06107

如果0-5年可以用算数平均算h,那最后一问为什么不用2-5年算数平均h来计算违约概率呢?