NO.PZ202304040200002103

问题如下:

An estimate of the ERP consistent with the Grinold-Kroner model is closest to:

选项:

A.2.7%.

3.0%.

4.3%.

解释:

B is correct.

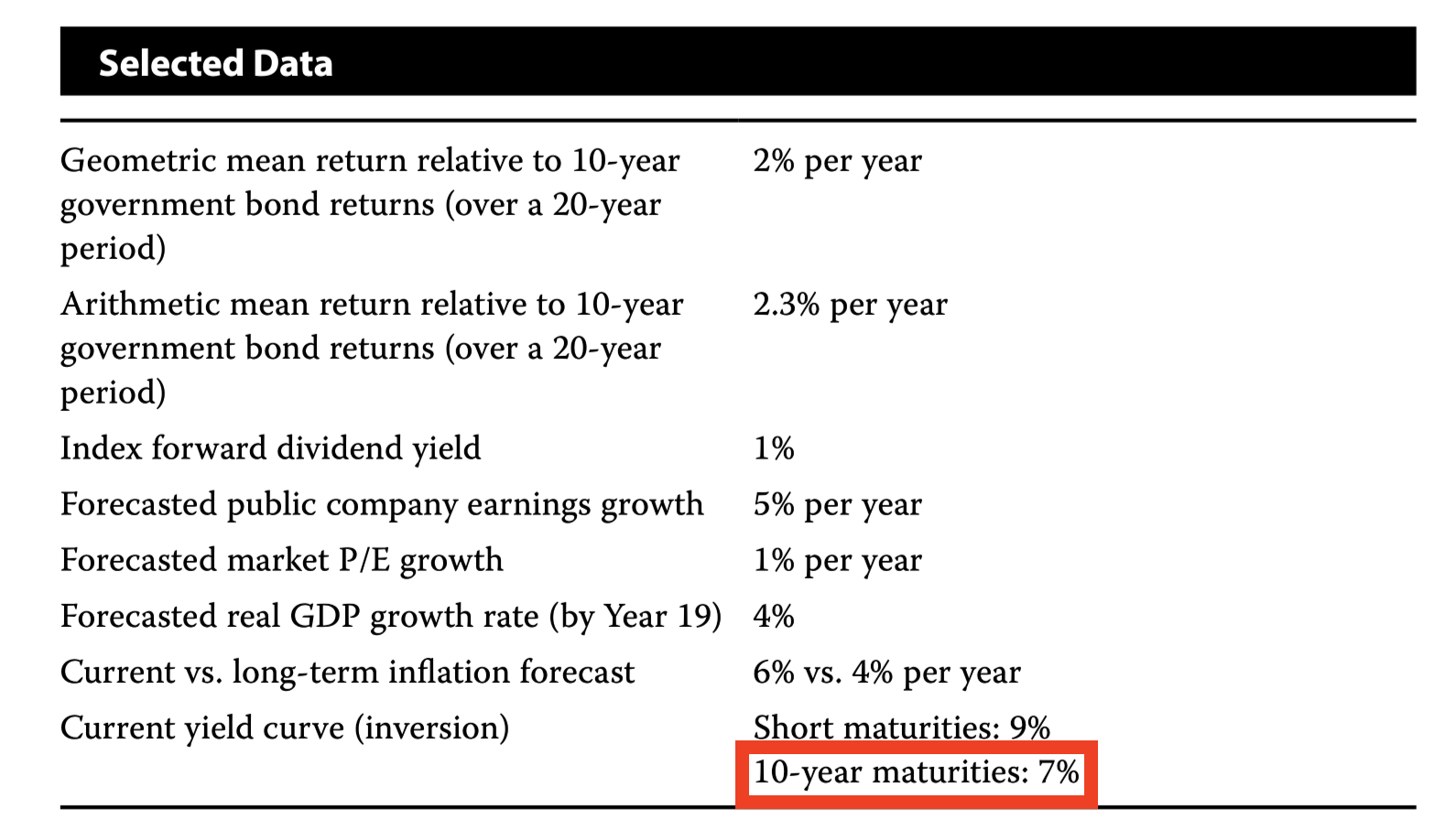

i = 4% per year (long-term forecast of inflation)

g = 4% per year (growth in real GDP)

Δ(P/E0 = 1% per year (growth in market P/E)

dy = 1% per year (dividend yield or the income portion)

Risk-free return = rf = 7% per year (for 10-year maturities)

Using the Grinold-Kroner model, the ERP estimate is

ERP = {1.0 + 1.0 +[4.0 + 4.0 + 0.0)] } – 7.0 = 3.0%.

The premium of 3.0% compensates investors for average market risk, given expectations for inflation, real earnings growth, P/E growth, and anticipated income.

老师,rf7%是怎么算出来的?题目里没看到这个数据。