NO.PZ2023040701000008

问题如下:

Let’s use the term structure of interest rates to price bonds, and in particular I want you to fully understand the relationships between spot and forward rates and yield to maturity. Use the data in Exhibit 1 to determine whether a 4% coupon Treasury bond, maturing in four years and offered by a dealer at a yield-to-maturity of 7.89% is cheap (buy recommendation), fairly valued (hold recommendation) or rich (sell recommendation) based on arbitrage opportunities.

Based on the data in Exhibit 1 and the yield to maturity quoted by the dealer, what action should an analyst most likely take with regard to the Treasury bond?

选项:

A.

Buy

B.

Hold

C.

Sell

解释:

Correct Answer: C

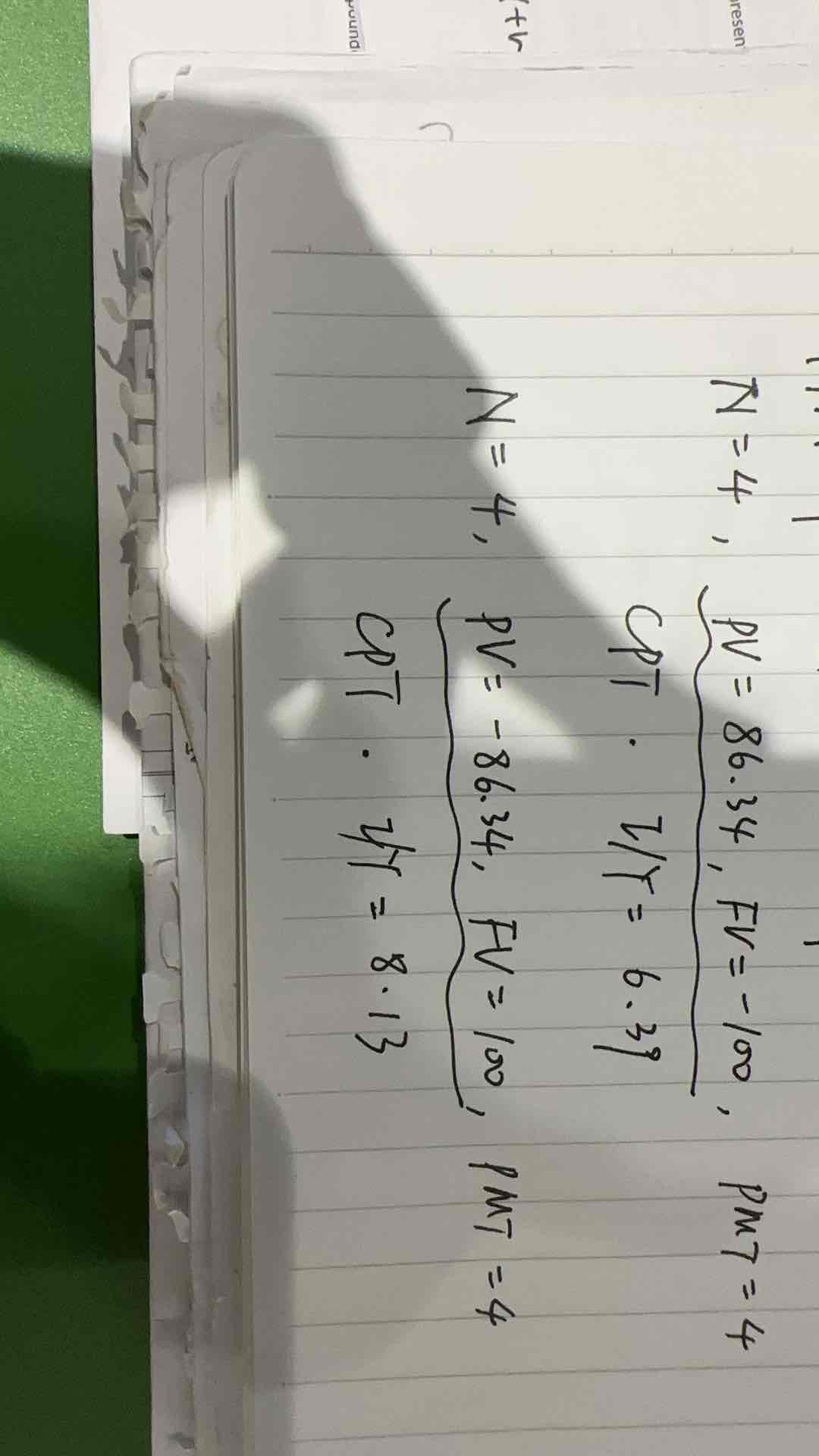

Since the quoted YTM of 7.89% is more expensive (price = $87.08) than the YTM based on the spot rates of 8.14% (price = $86.34), the analyst should sell the bond.

Step 1: Calculate the year 3 rate from the discount factor.

Step 2: Using the year 3 spot rate and the forward rate f(2,1), calculate the year 2 spot rate.

Step 3: Using the spot rates, calculate the YTM for the bond using your calculator.

YTM = 8.14%.

Step 4: Since the quoted YTM of 7.89% is more expensive (price = $87.08) than the YTM based on the spot rates of 8.14% (price = $86.34), the analyst should sell the bond.

不明白为什么结果不同