o.PZ2019052801000039 (选择题)来源: 品职出题

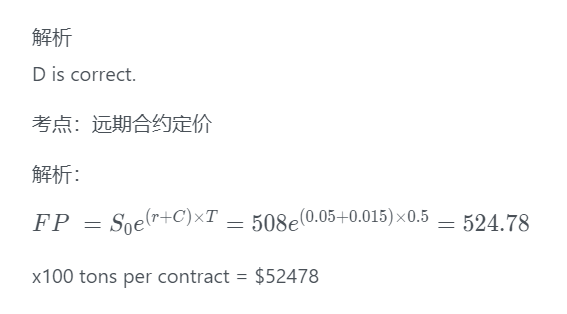

A farmer plans to sell 50,000 tons of soybeans in six months, he decides to short futures contracts to hedge against the price deline. The current price of soybeans is $ 508/ton, the contract size is 100 tons, the storage cost for the soybeans is 1.5% per year. The continuously compounded rate is 5%, what's the price for the futures contract ?

这是我自己画图解答的过程,问题如图,为什么cost折现到t=0时刻,是用S0乘以百分比,不是除以?

此外,我还有个疑问,如果是long position出现cost,那么cost折现到t=0时刻,是用FP除以还是乘以?

到底是除还是乘百分比,这个怎么确认?