NO.PZ202206210100000301

问题如下:

From the description of Sabonete’s objectives for the SPP, the most appropriate asset allocation approach is:

选项:

A.mean–variance optimization. B.a basic two-portfolio approach. C.an integrated asset–liability approach.解释:

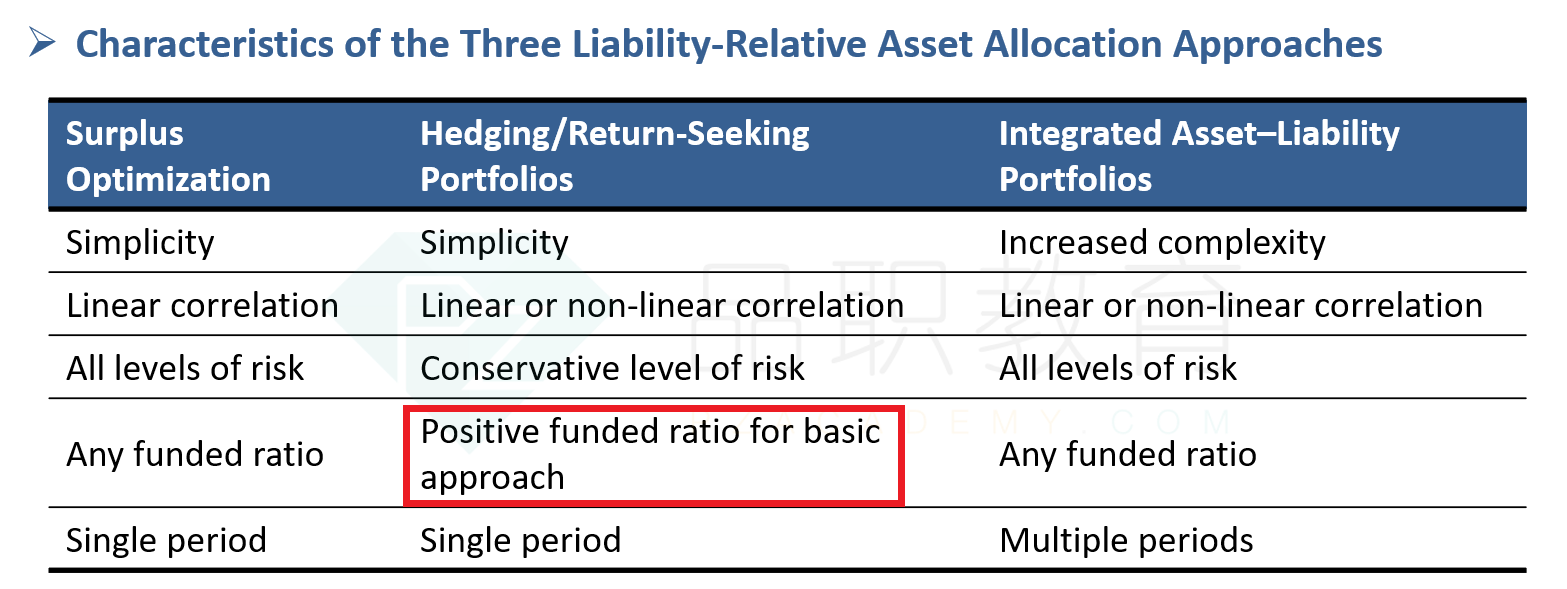

SoluC is correct. Based on the objectives described, the integrated asset–liability approach is the most appropriate asset allocation approach for the SPP, which is currently under-funded and seeks to achieve fully funded status in five years. Mean–variance optimization is an asset-only approach to asset allocation and fails to consider Sabonete’s goal of fully funding the liabilities. The basic two-portfolio approach assumes the pension plan has a surplus that can be allocated to a return-seeking portfolio.

C is correct. Based on the objectives described, the integrated asset–liability approach is the most appropriate asset allocation approach for the SPP, which is currently under-funded and seeks to achieve fully funded status in five years. Mean–variance optimization is an asset-only approach to asset allocation and fails to consider Sabonete’s goal of fully funding the liabilities. The basic two-portfolio approach assumes the pension plan has a surplus that can be allocated to a return-seeking portfolio.

A is incorrect. Mean–variance optimization is an asset-only approach to asset allocation and fails to consider Sabonete’s goal of fully funding the liabilities.

B is incorrect. The basic two-portfolio approach assumes the pension plan has a surplus that can be allocated to a return-seeking portfolio.

看了助教们的解释,依然不理解B和C。

B的方法,讲义上也说可以under funded情况呀,为什么直接就排除了呢?。另外从我们正常做题角度来看,肯定都是顺着题目,现在是需要通读全文才能判断题目吗?

我发现三级课后题目,很多答题对应的信息点都不像2级,很多前前后后都有,考试也是吗