NO.PZ202208220100000403

问题如下:

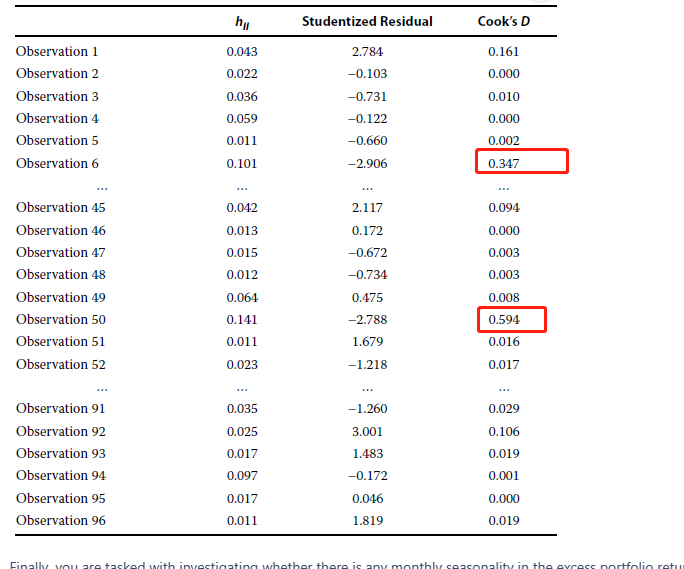

The CIO asks you to analyze one of the firm’s portfolios to identify influential outliers that might be skewing regression results of its return drivers. For each observation, you calculate leverage, the studentized residual, and Cook’s D.There are 96 observations and two independent variables (k = 2), and the criticalt-statistic is 2.63 at a 1% significance level. Partial results of your calculations areshown in Exhibit 1.

Finally, you are tasked with investigating whether there is any monthly seasonality in the excess portfolio returns. You construct a regression model using dummy variables for the months; your regression statistics and ANOVA results are shown in Exhibit 2.

Determine and justify the potentially influential observations in Exhibit 1 using the criteria for Cook’s D involving k and n.

选项:

A.Observations 6 and 50, because their Cook’s D values exceed 0.144

B.Observations 6 and 50, because their Cook’s D values exceed 0.289

C.Observations 1, 6, 50, and 92, because their Cook’s D values exceed 0.100

解释:

B is correct. The required criteria for using Cook’s D to identify influential observations is

which implies the ith observation is highly likely to be an influential data point. Since n = 96 and k = 2, then  = 0.289. Only two observations, 6 and 50, have a Cook’s D that exceeds 0.289, so they are highly likely to be influential observations.

= 0.289. Only two observations, 6 and 50, have a Cook’s D that exceeds 0.289, so they are highly likely to be influential observations.

6和50是怎么来的?

这个0.289进行比较得到的哦。我们发现只有6和50的这个D值大于0.289,所以他们两是最有可能为influential observations.

这个0.289进行比较得到的哦。我们发现只有6和50的这个D值大于0.289,所以他们两是最有可能为influential observations.