NO.PZ2019122802000017

问题如下:

Sushil Wallace is the chief investment officer of a large pension fund. Wallace wants to increase the pension fund’s allocation to hedge funds and recently met with three hedge fund managers. These hedge funds focus on the following strategies:

Hedge Fund A: Specialist—Follows relative value volatility arbitrage

Describe three paths for implementing the strategy of Hedge Fund A.

解释:

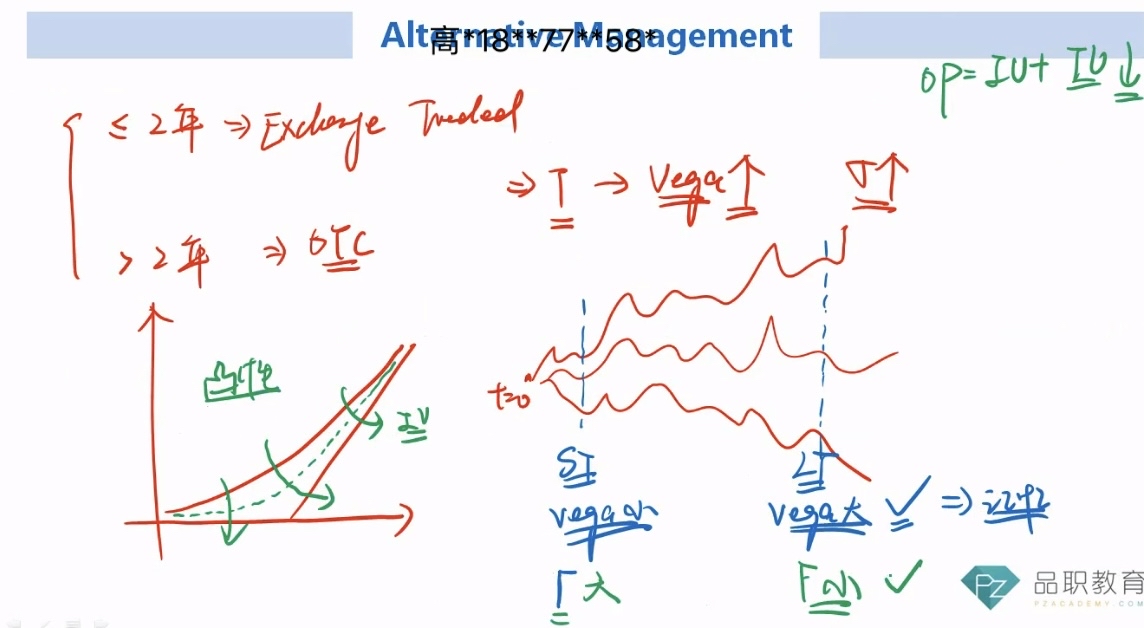

Hedge Fund A’s volatility trading strategy can be implemented by following multiple paths. One path is through simple exchange-traded

options. The maturity of such options typically extends to no more than

two years. In terms of expiry, the longer-dated options will have more

absolute exposure to volatility levels than shorter-dated options, but

the shorter-dated options will exhibit more delta sensitivity to price

changes.

A second, similar path is to implement the volatility

trading strategy using OTC options. In this case, the tenor and strike

prices of the options can be customized. The tenor of expiry dates can

then be extended beyond what is available with exchange-traded options.

A

third path is to use VIX futures or options on VIX futures as a way to

more explicitly express a pure volatility view without the need for

constant delta hedging of an equity put or call for isolating the

volatility exposure.

A fourth path for implementing a volatility

trading strategy would be to purchase an OTC volatility swap or a

variance swap from a creditworthy counterparty. A volatility swap is a

forward contract on future realized price volatility. Similarly, a

variance swap is a forward contract on future realized price variance,

where variance is the square of volatility. Both volatility and variance

swaps provide “pure” exposure to volatility alone, unlike standardized

options in which the volatility exposure depends on the price of the

underlying asset and must be isolated and extracted via delta hedging.

首先只要Specialist— relative value volatility arbitrage,都是short波动率低,long波动率高的,进行套利。这四种都是,只是这四种都有各自的特点,首先就是策略一和策略二都受到delta和gamma的影响(所以要想办法对冲掉),策略三和四不受影响。

策略一是通过简单的交易所交易期权。这类期权的到期时间一般不超过两年。从到期日来看,期限较长的期权比期限较短的期权对波动率水平的绝对风险敞口更大,所以是long长期short短期,但期限较短的期权对价格变化表现出更多的delta敏感性,所以对冲掉delta。

策略二类似的路径是利用场外期权实施波动率交易策略。在这种情况下,期权的期限和行权价格可以自定义。然后,到期日的期限可以扩展到交易所交易的期权之外。但是会有counterpart risk的风险。

对冲掉delta和gamma方法,delta对冲很简答,delta是一阶导,说白了就是同涨同跌,如果delta是,1,那就是stock涨了10,option涨了10,有十张call就做空10股stock,如果是-1,比如put,有十张put,那就做多10股stock。

至于gamma,假设100股C股票涨了1%,然后*100股,就涨了100对吧,而买的这个C股票的call因为gamma的原因没有百分百的对冲,涨了1.2%,对应就是涨了120对吧。那现在多了120-100=20,就卖空20股C股票,这样就100%的对冲了。

relative value volatility arbitrage实际就是套利,赚取spread,做空高估volatility的,做多类似的低估volatility。但是有的(比如策略一和策略二,的期权)实施这个策略会有delta和gamma的影响(大概说下就是期权会有方向性的delta和二阶导的gamma等因素影响),但是我不想受除了volatility以外的因素影响,就需要借助工具对冲掉,对吧,但是一般都不能完全对冲干净其它影响因素,这样套利就很受影响。这里策略三 实际VIX Index futures (or options on VIX futures),本质就是一个专门交易volatility的index的future或者volatility的index的future的期权(有点绕口,可以理解就是前面的future为底层资产的option)。因为只交易volatility,所以影响因素只有volatility,这时候,就只考虑做多低估的volatility的future做空类似的高估的volatility的future。而不用担心受到delta和gamma的影响了。

策略四实际就是互换,用现在的波动换将来的波动率,这个好理解。

所以st 的option vega小 gamma大 delta 大?

这段不需要背吗?