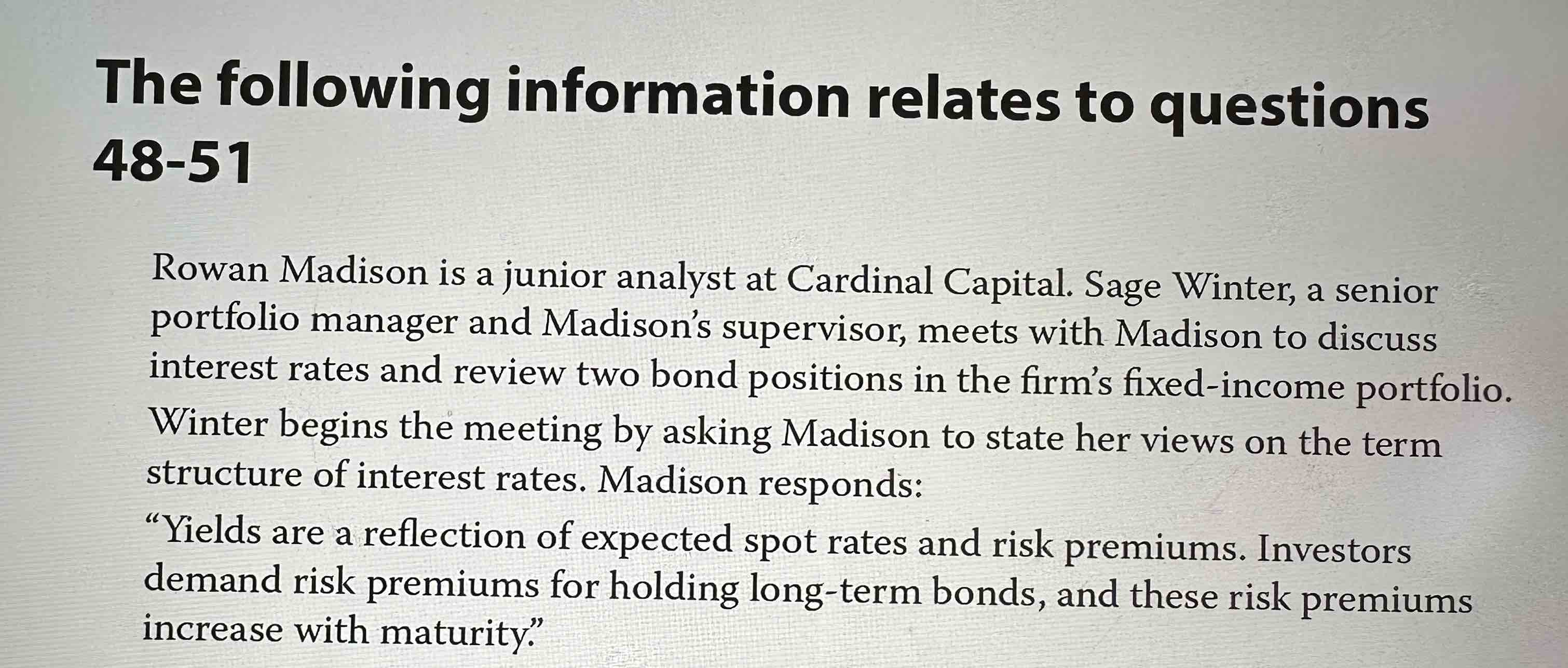

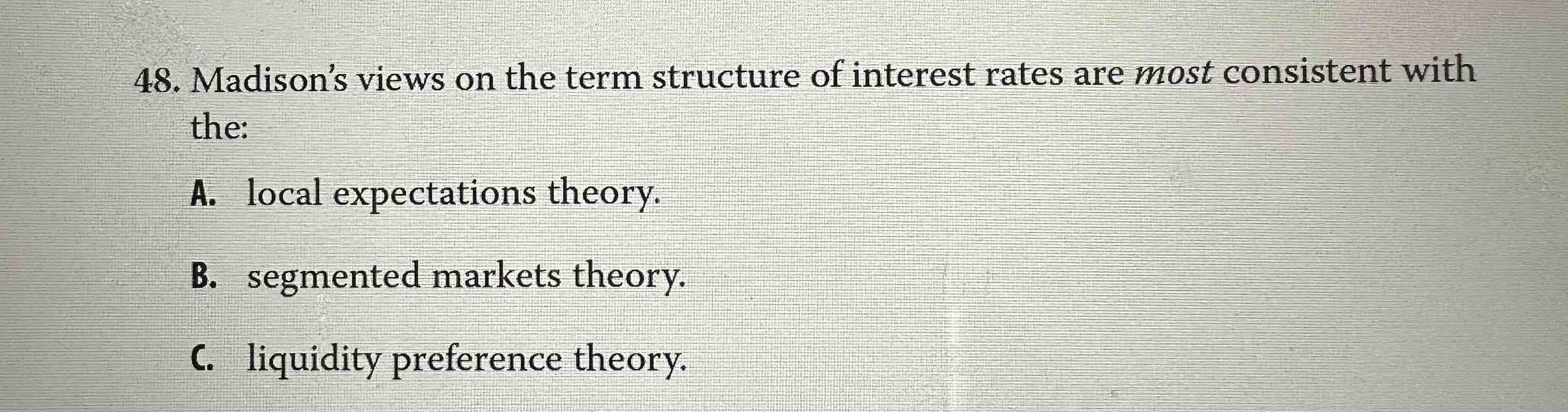

题目里问的是risk premium 而不是liquidity premium,为什么不选local expectations theory? 他的定义不是LT需要risk premium,而liquidity premium theory不是LT需要liquidity premium吗?

吴昊_品职助教 · 2023年05月22日

嗨,努力学习的PZer你好:

前半段的描述中,说yields反映了expected spot rate和risk premiums,并没有很明确的说明是短期还是长期。local expectation theory中,短期是风险中性的,只有长期存在risk premium。

再者,他的描述中后半段说风险溢价随着时间增长,可以确定是liquidity premium。local expectation theory只是说明短期是风险中性的,长期投资有补偿,并没有说风险补偿随时间增加。

----------------------------------------------就算太阳没有迎着我们而来,我们正在朝着它而去,加油!