NO.PZ201712110100000209

问题如下:

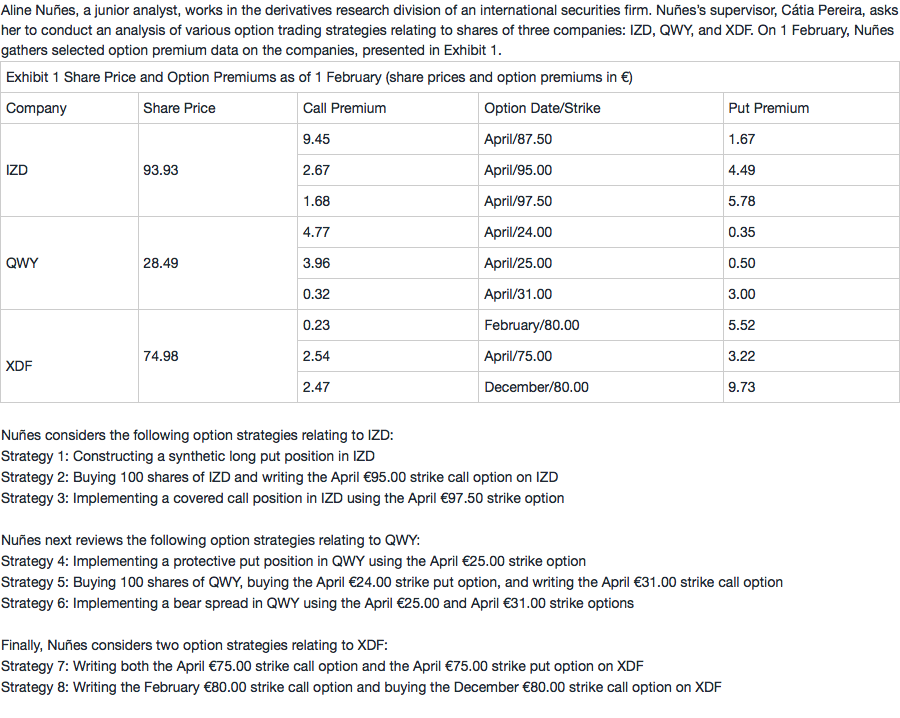

Based on Exhibit 1, the best explanation for Nuñes to implement Strategy 8 would be that, between the February and December expiration dates, she expects the share price of XDF to:

选项:

A.

decrease.

B.

remain unchanged.

C.

increase.

解释:

C is correct.

Nuñes would implement Strategy 8, which is a long calendar spread, if she expects the XDF share price to increase between the February and December expiration dates. This strategy provides a benefit from the February short call premium to partially offset the cost of the December long call option. Nuñes likely expects the XDF share price to remain relatively flat between the current price €74.98 and €80 until the February call option expires, after which time she expects the share price to increase above €80. If such expectations come to fruition, the February call would expire worthless and Nuñes would realize gains on the December call option.

中文解析:

本题考察的是calendar spread策略。

策略8中,卖出了2月份到期的看涨期权,买入12月份到期的看涨期权。说明他认为在目前到2月份这段时间内股价是稳定的,波动很小;但是在2月份到12月份期间股价将会上涨。所以选C。

对于calendar spread。主要是判断两点:

1. 判断短期和长期波动率的大小来确定long 和short 的头寸,例如,预测短期平稳,长期波动大就long calendar;预测短期波动大,长期平稳就short calendar

2. 判断使用call还是put来构建,主要是看预测将来股价上涨还是下跌,预测上涨就用call构建,预测下跌就用put来构建

通过上面两步就可以最终确定如何构建calendar 头寸了。

2月期权不应该是针对未来,即针对2月以后行情的预期表达吗?如果是针对2月前的情况,都发生了,变成实际情况了,买期权还有什么用呢?