NO.PZ202206210100000306

问题如下:

Which of the following statements is the best response to D’Alessandro’s rationale for justifying Option 1 for the SPP’s asset allocation? The proposed model:选项:

A.is not well suited to the SPP given its objective of fully funding and hedging its liabilities. B.would benefit the SPP because it can be expected to generate higher returns, more than offsetting the higher costs. C.has an inherent illiquidity premium, which will help Sabonete achieve its objective of fully funding the pension plan.解释:

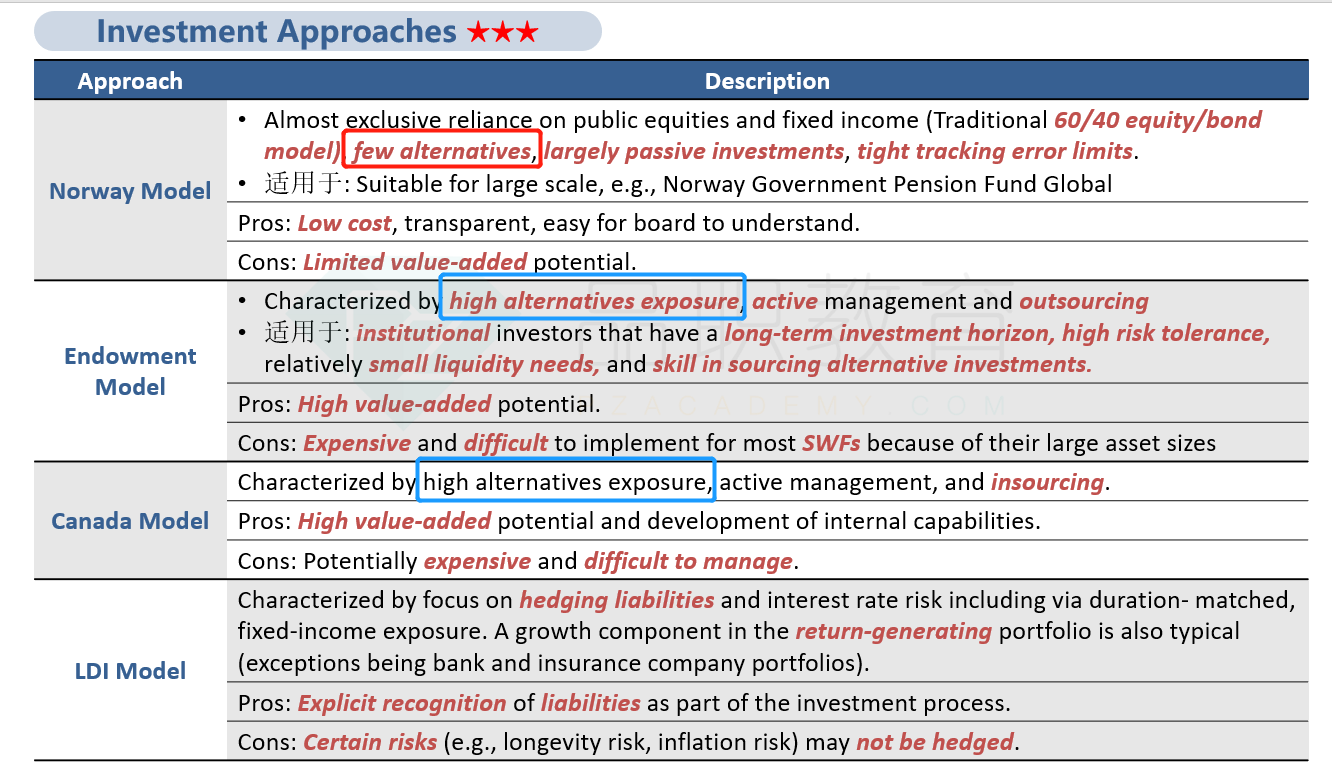

SolutionA is correct. D’Alessandro suggests that the endowment model should be used by the pension plan. The endowment model is not well suited to meeting Sabonete’s objectives. The model seeks to earn illiquidity premiums, which require a long-time horizon to capture. Because Sabonete plans to hedge its liabilities in five years, its investment horizon is too short to capture the illiquidity premium that is a critical component of the endowment model.

B is incorrect. The endowment model can be expected to generate higher returns because of the illiquidity premium, which would more than offset the higher costs. However, Sabonete’s investment horizon is too short to capture the illiquidity premium inherent in the model. Further, the higher costs of the model are inconsistent with Sabonete’s desire to minimize the investment and administrative costs associated with the plan.

C is incorrect. Sabonete’s investment horizon is too short to capture the illiquidity premium that is a critical component of the endowment model. Further, the higher costs of the model are inconsistent with Sabonete’s objective to minimize the investment and administrative costs associated with the plan.

A is correct. D’Alessandro suggests that the endowment model should be used by the pension plan. The endowment model is not well suited to meeting Sabonete’s objectives. The model seeks to earn illiquidity premiums, which require a long-time horizon to capture. Because Sabonete plans to hedge its liabilities in five years, its investment horizon is too short to capture the illiquidity premium that is a critical component of the endowment model.

investment horizon不是五年吗?怎么会太短呢?