这道题想考什么没看懂呢🥹

品职答疑小助手雍 · 2023年05月13日

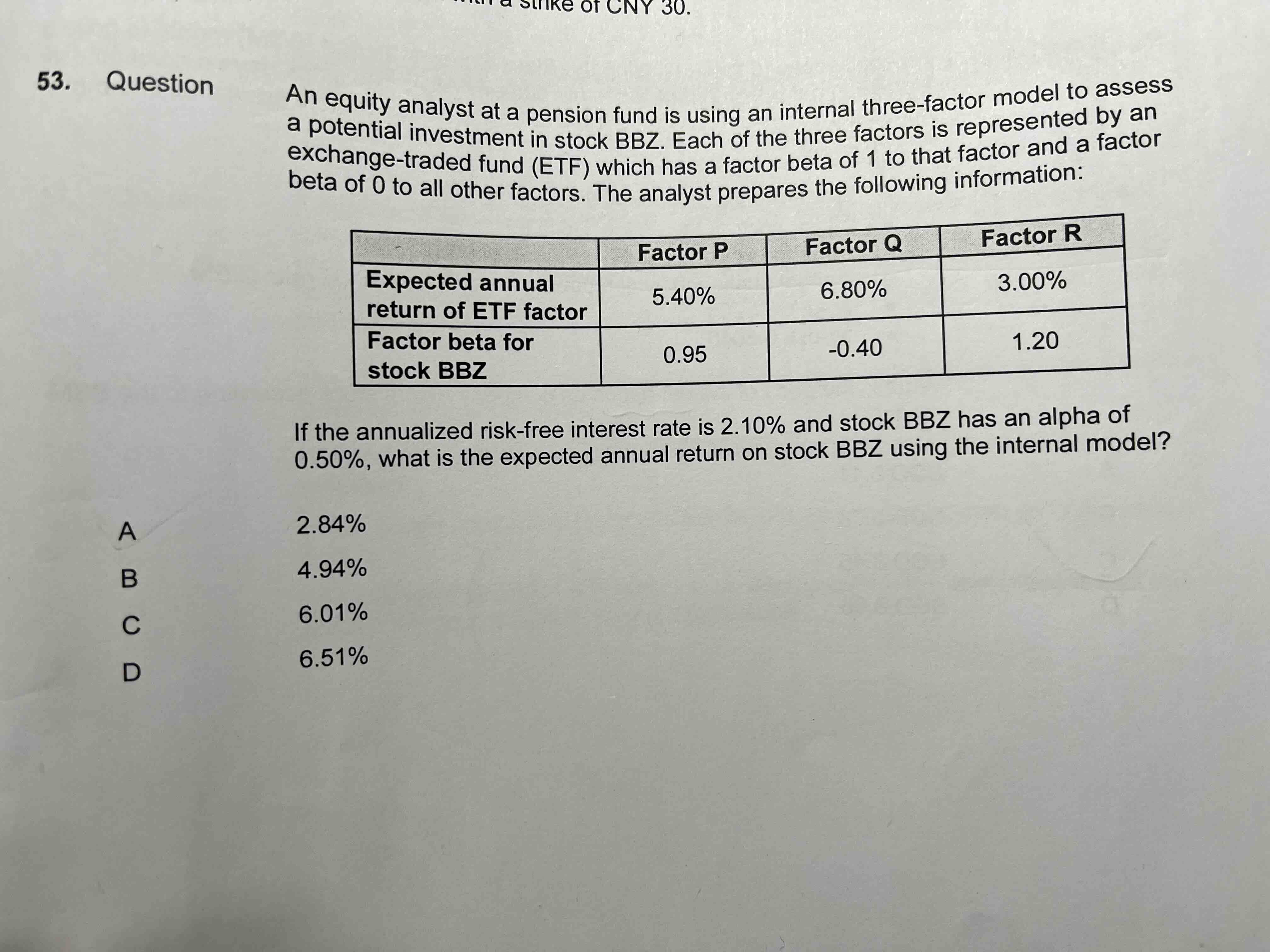

同学你好,这题中间有一句Each of the three factors is represented by anexchange-traded fund (ETF) which has a factor beta of 1 to that factor and a factor beta of 0 to all other factors.我觉得大致意思就是让套用capm的Rm了,只不过有3个参考基准的Rm。就很像Fama-French的三因素模型那样,只不过后面两个因素不是市值而是其他的Rm。

所以就相当于b1(Rm1-rf)+b2(Rm2-rf)+b3(Rm3-rf)+a。