NO.PZ2019120301000271

问题如下:

Question

A company that prepares its financial statements according to IFRS leased a piece of equipment on 1 January 2020. Information relevant to the transaction is as follows:

Five annual lease payments of $25,000, with the first payment due 1 January 2020

Interest rate on similar company debt is currently 8%

The fair value of the equipment is $115,000

Useful life of the equipment is seven years

The company depreciates other equipment in the same asset class on a straight-line basis

The total expense related to the lease on the company’s 2020 income statement will be closest to:

选项:

A.$25,000.00 B.$28,185.00 C.$22,024.00解释:

Solution

B is correct. Under IFRS 16 all leases are classified as a finance lease and must be capitalized.

Using a financial calculator for an annuity due at the beginning of the period:

PV of lease payments: PMT = $25,000, i = 8%, N = 5, Mode = Begin, Compute PV.

PV = $107,803

Therefore, the lease would be capitalized at $107,803.

A is incorrect. It assumes it is an operating lease and simply deducts the lease payment.

C is incorrect. It correctly classifies it as a finance lease but amortizes it over 7 years: 107,803/7 = 15,400; 15,400 + 6,624 = 22,024.

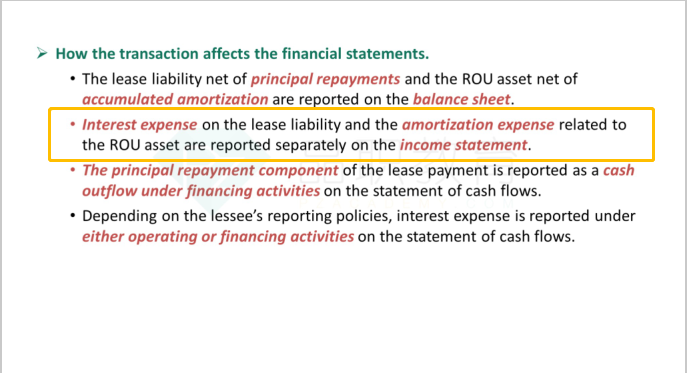

请问老师:本题计算摊销费用为何使用lease term,而非使用equipment的useful life?这个摊销不是针对ROU的吗?这种摊销方式是会计准则的规定吗?