NO.PZ2020011303000057

问题如下:

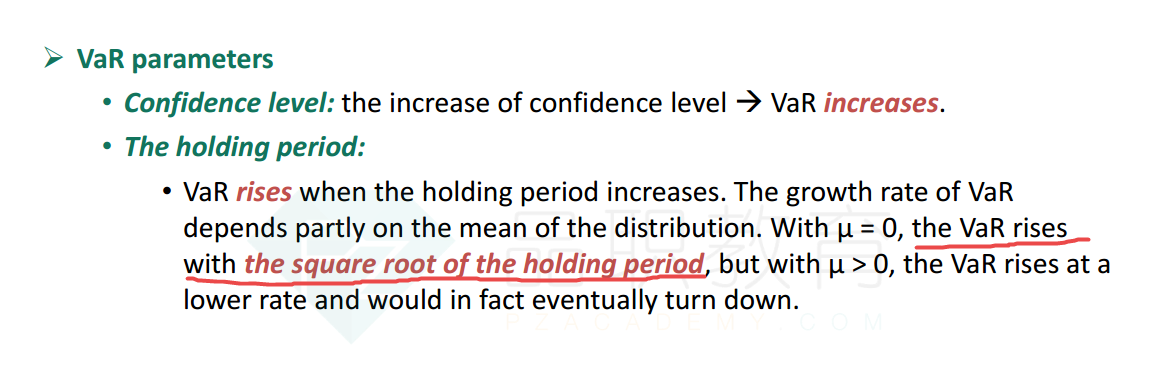

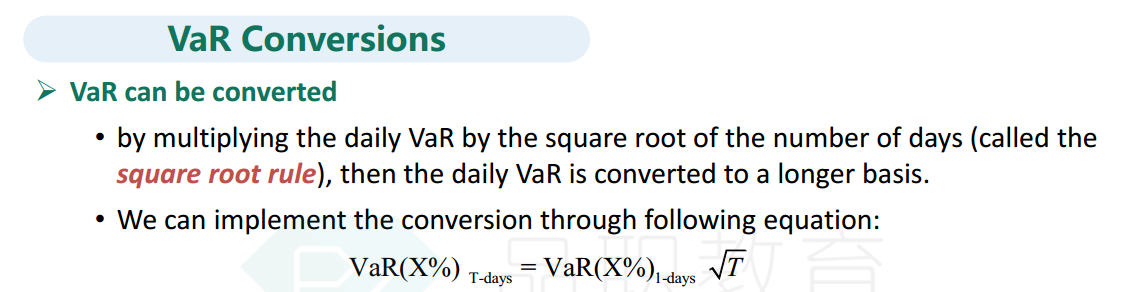

What is the relationship usually assumed between the VaR with 99% confidence for a ten-day time horizon and the VaR with 99% confidence for a one-day time horizon?

解释:

The ten-day VaR is the square root of 10 multiplied by the one-day VaR.

99%10天的VaR和99%1天的VaR有什么关系?

99%10天的VaR=10^0.5*99%1天的VaR

这是为什么。。。。。