NO.PZ2022062759000005

问题如下:

The collapse of Long-Term Capital Management (LTCM) is a classic risk management case study. Which of the

following statements about risk management at LTCM is correct?

选项:

A.

LTCM’s traders did not respond quickly enough to changes in market volatility as there were significant

barriers that blocked the flow of information.

B.

LTCM failed to account for the illiquidity of its largest positions in its risk calculations.

C.

LTCM’s use of high leverage is evidence of poor risk management.

D.

LTCM did not run any stress scenarios on its VaR model.

解释:

中文解析:

关于长期资本管理公司的失败,是由于大额头寸的流动性不足所造成的。

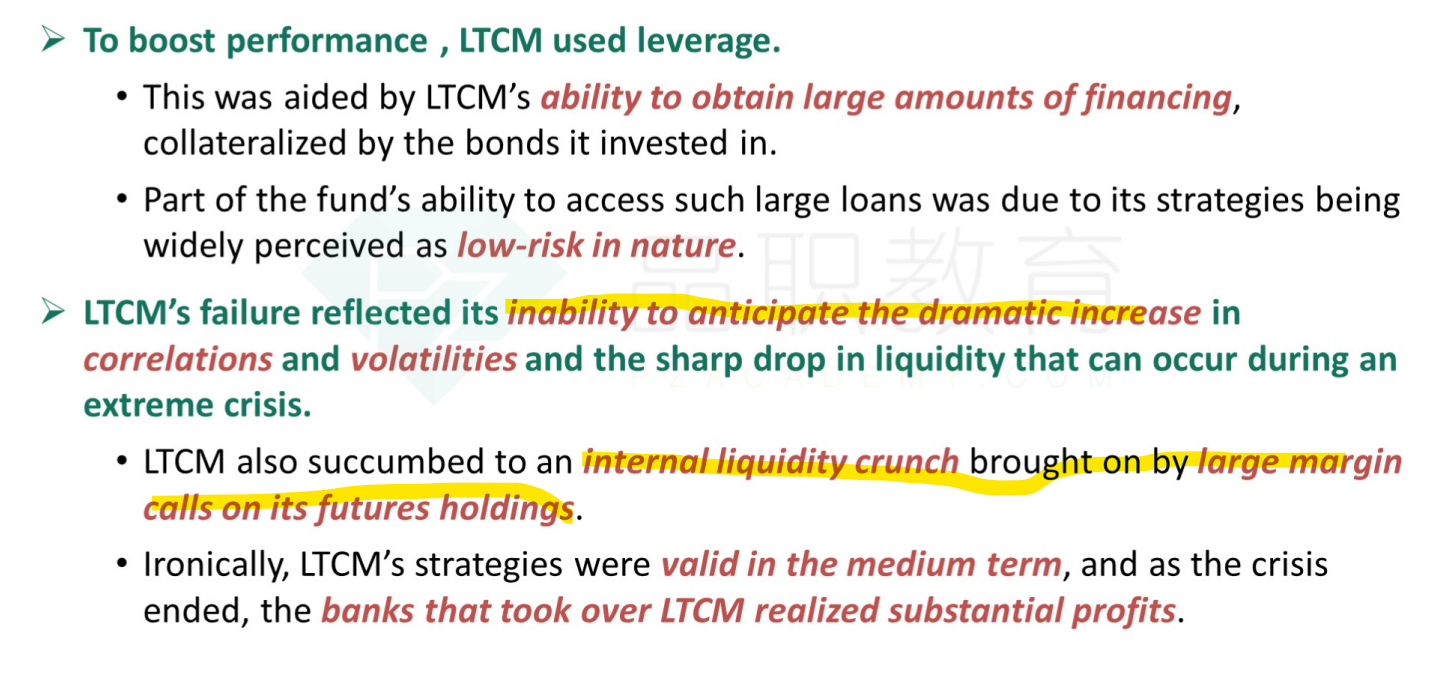

A major contributing factor to the collapse of LTCM is that it did not account properly for the illiquidity of its largest positions in its risk calculations. LTCM received valuation reports from dealers who only knew a small portion of LTCM’s total position in particular securities, therefore understating LTCM’s true liquidity risk. When the markets became unsettled due to the Russian debt crisis in August 1998 and a separate firm decided to liquidate large positions which were similar to many at LTCM, the illiquidity of LTCM’s positions forced it into a situation where it was reluctant to sell and create an even more dramatic adverse market impact even as its equity was rapidly deteriorating. To avert a full collapse, LTCM’s creditors finally stepped in to provide USD 3.65 billion in additional liquidity to allow LTCM to continue holding its positions through the turbulent market conditions in the fall of 1998.

However, as a result, investors and managers in LTCM other than the creditors

themselves lost almost all their investment in the fund.

d怎么不对咯?不就是极端情况下相关系数风险吗?