NO.PZ2016082404000038

问题如下:

An option on the Bovespa stock index is struck on 3,000 Brazilian reais (BRL). The delta of the option is 0.6, and the annual volatility of the index is 24%. Using delta-normal assumptions, what is the 10-day VAR at the 95% confidence level? Assume 260 days per year.

选项:

A.

44 BRL

B.

139 BRL

C.

2,240 BRL

D.

278 BRL

解释:

ANSWER: B

The linear VAR is derived from the worst move in the index value, which is . Multiplying by the delta of 0.6 gives 139.

解析:

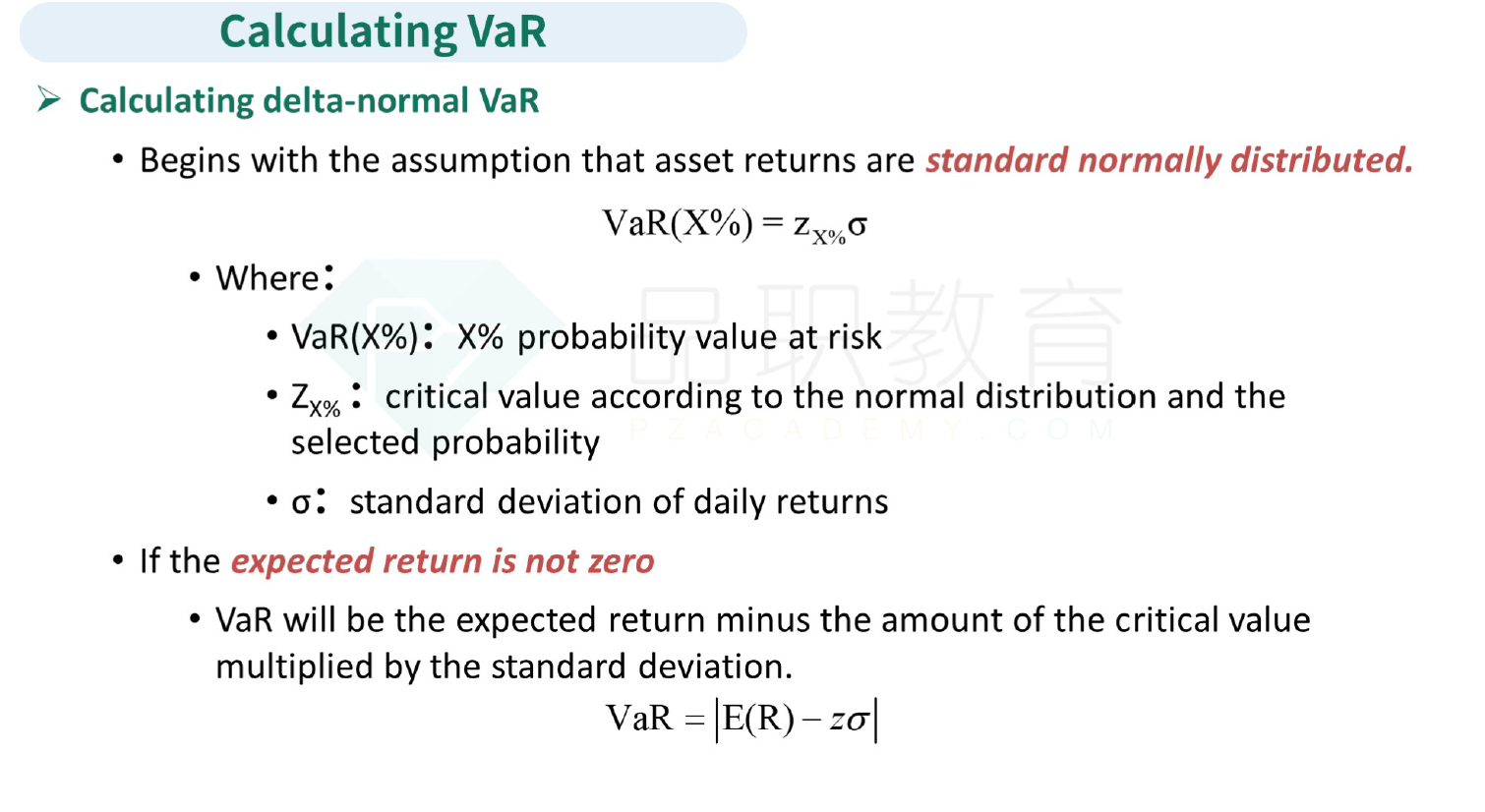

现在有一个以股票index为基础资产的option价格为3000BRL,delta=0.6,年化σ=24%,用delta-normal的假设,求20天95%的VaR是多少?假设一年260天

95%置信区间对应的Z值=1.645

VaR=Z*S*delta*σ*区间调整

=1.645*3000*0.6*24%/(260^0.5)*(10^0.5)=139

请问这个计算都用到哪几个知识点和哪几个公式?