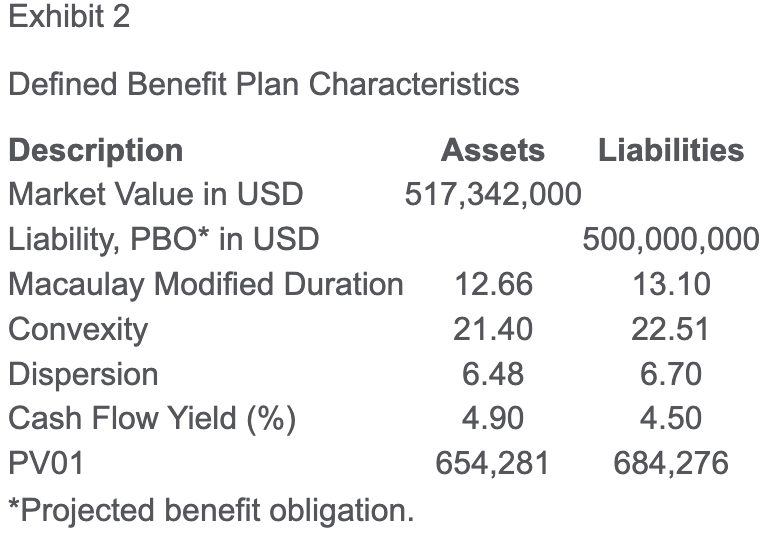

Silver and Shrewsbury begin discussing a client that sponsors a US DB plan. The client wants to immunize the liabilities such that changes in interest rates under various scenarios will not cause a deterioration in funded status. Key data for the plan assets and liabilities are provided in Exhibit 2. Silver’s forecast is that interest rates will rise in a non-parallel fashion. In fact, he expects a bear steepening of the curve as inflation accelerates because of rising wages.

Based on the data in Exhibit 2, will the client discussed most likely be able to immunize its DB plan given the interest rate scenario described by Silver?

- Yes

- No, because of the differences in money duration

- No, because of the differences in convexity and dispersion

老师您好,想请教下如何理解这道题,这道题是不是不满足Convexity A>L?