NO.PZ2022071105000011

问题如下:

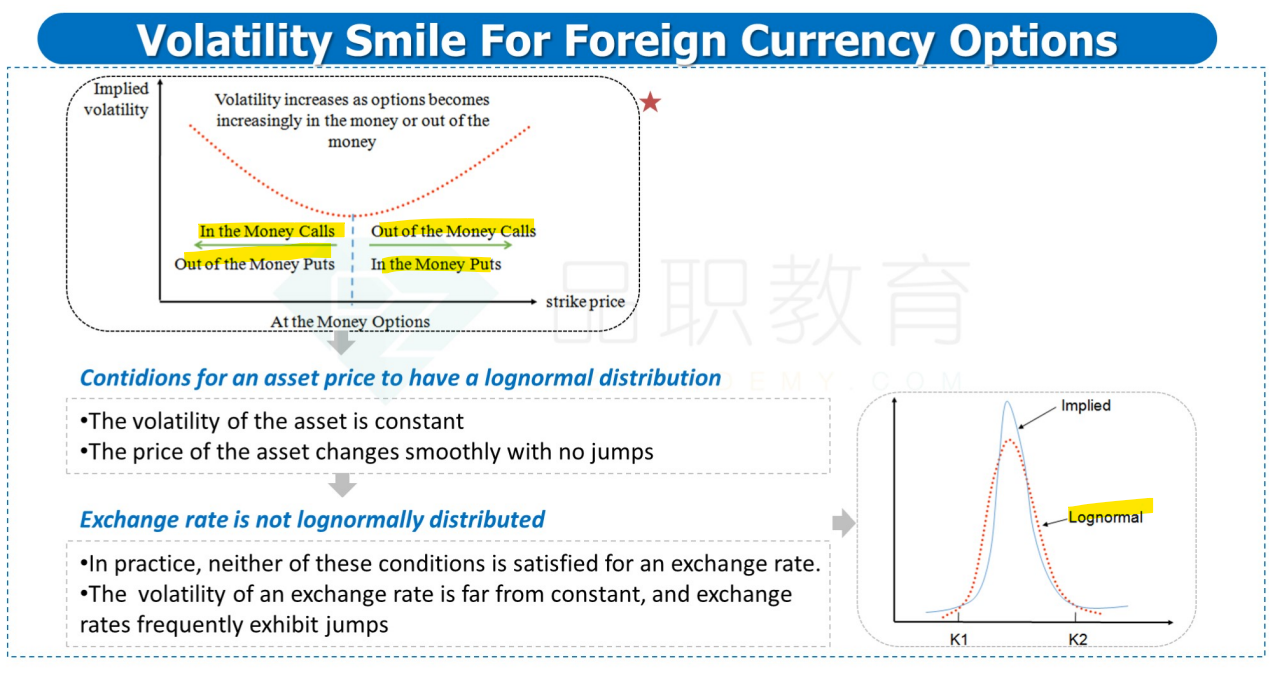

A risk analyst is examining a firm’s foreign currency option pricing assumptions. The implied volatility is

relatively low for an at-the-money option and it becomes progressively higher as the option moves either in-

the-money or out-of-the-money. How does the distribution of option prices on this foreign currency implied by

the Black-Scholes-Merton model compare to the lognormal distribution with the same mean and standard

deviation?

选项:

A.It has a heavier left tail and a less heavy right tail.

B.It has a heavier left tail and a heavier right tail.

C.It has a less heavy left tail and a heavier right tail.

D.It has a less heavy left tail and a less heavy right tail.

解释:

中文解析:

B是正确的。对于一个外币期权,隐含的分布给出了一个相对较高的期权价格。平值期权的隐含波动率相对较低,但是

当它转变为价内或价外期权时,隐含波动率就会升高。因此隐含的分布比对数正态分布具有更厚的尾部。

B is correct. For a foreign currency option, the implied distribution gives a relatively high

price for the option. The implied volatility is relatively low for at-the-money options, but

it becomes higher as the option moves either in-the-money or out-of-the-money. Thus,

the implied distribution has heavier tails than the lognormal distribution.

老师您好,我有点没明白,平日学的那个lognormal 表现为双瘦尾和这道题的区别在哪里。什么叫转换为价外期权,答案没整明白。麻烦老师了