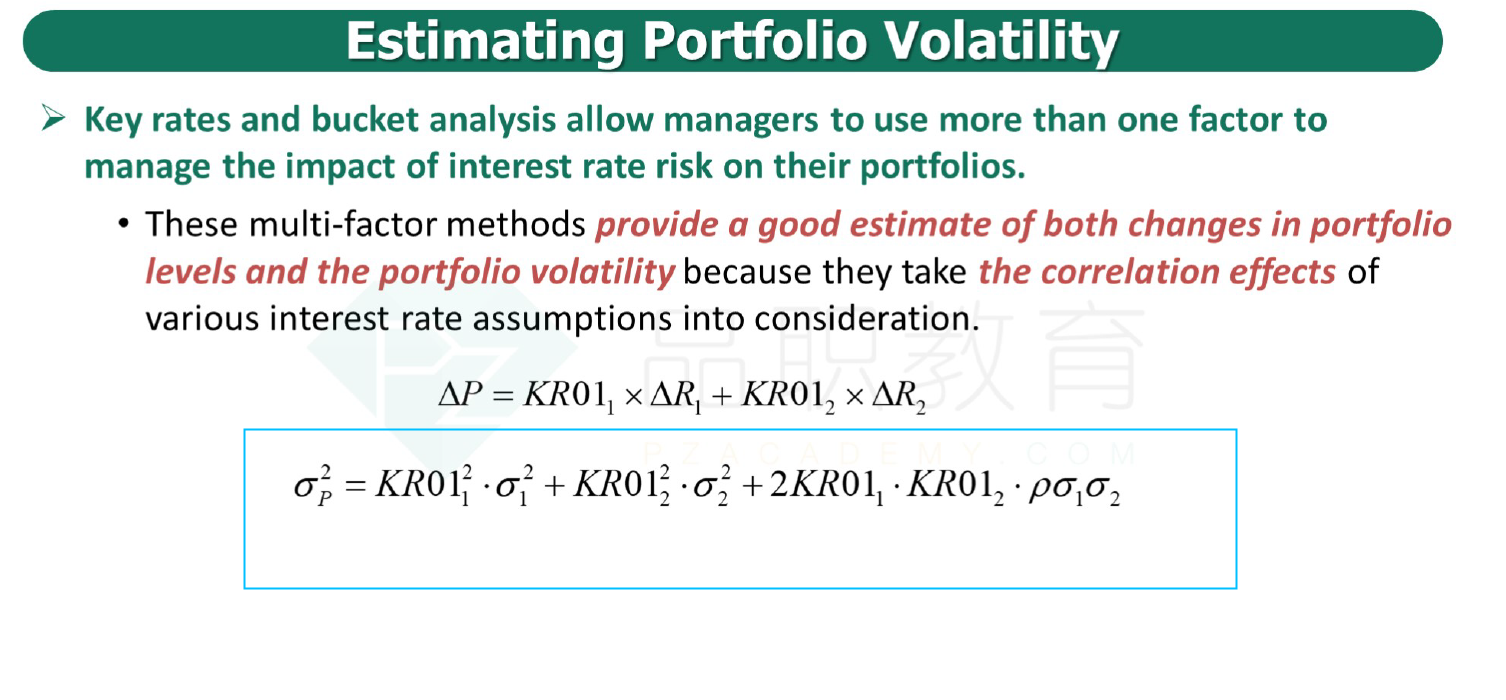

问题如下:

The CRO of a small bank is estimating the volatility of the bank’s asset portfolio using its key rate 01s, in preparation for calculating the bank’s market risk capital. The portfolio is only exposed to 2-year and 10-year spot rates. Relevant information on market rates and the portfolio is as follows:

Given the above information, what is the standard deviation of the daily change in portfolio value?

选项:

A.

CAD 516

B.

CAD 988

C.

CAD 1,026

D.

CAD 1,203

解释:

中文解析:

D是正确的。资产组合的价值变动的方差计算如下:

σP2=∑i=1n∑j=1nρijσiσj∗KR01i∗KR01j

=(1∗σ2Y∗σ2Y∗KR012Y∗KR012Y)+(ρ2Y,10Y∗σ2Y∗σ10Y∗KR012Y∗KR0110Y)

+(ρ10Y,2Y∗σ10Y∗σ2Y∗KR0110Y∗KR012Y)

+(1∗σ10∗σ10Y∗KR0110Y∗KR0110Y)

=σ2Y2∗KR012Y2+2∗(1∗σ2Y∗σ2Y∗KR012Y∗KR012Y)+σ102∗KR0110Y2

=[(4)2∗(52)2]+[0.6∗4∗11∗52∗97]+[0.6∗11∗4∗97∗52]+[(11)2∗(97)2]

=1,448,076

所以标准差=√1,448,076 = 1,203.36.

---------------------------------------------------------------------------------------------------------------------

D is correct. The equation for the variance of the change in portfolio value is:

σP2=∑i=1n∑j=1nρijσiσj∗KR01i∗KR01j

=(1∗σ2Y∗σ2Y∗KR012Y∗KR012Y)+(ρ2Y,10Y∗σ2Y∗σ10Y∗KR012Y∗KR0110Y)

+(ρ10Y,2Y∗σ10Y∗σ2Y∗KR0110Y∗KR012Y)

+(1∗σ10∗σ10Y∗KR0110Y∗KR0110Y)

=σ2Y2∗KR012Y2+2∗(1∗σ2Y∗σ2Y∗KR012Y∗KR012Y)+σ102∗KR0110Y2

=[(4)2∗(52)2]+[0.6∗4∗11∗52∗97]+[0.6∗11∗4∗97∗52]+[(11)2∗(97)2]

=1,448,076

The standard deviation is therefore: √1,448,076 = 1,203.36.

A is incorrect. This calculates the variance as

= [0.6 ∗ 4 ∗ 11 ∗ 52 ∗ 97] + [0.6 ∗ 11 ∗ 4 ∗ 97 ∗ 52].

B is incorrect. This calculates the variance as

= [0.6 ∗ 4^2 ∗ 52^2 ] + [0.6 ∗ 11^2 ∗ 97^2 ].

C is incorrect. This calculates the variance without the KR01 terms, and then multiplies

the result by the average of the KR01s.