NO.PZ2016082402000047

问题如下:

From the time of issuance until the bond matures, which of the following bonds is most likely to exhibit negative convexity?

选项:

A.

A puttable bond

B.

A callable bond

C.

An option-free bond selling at a discount

D.

A zero-coupon bond

解释:

ANSWER: B

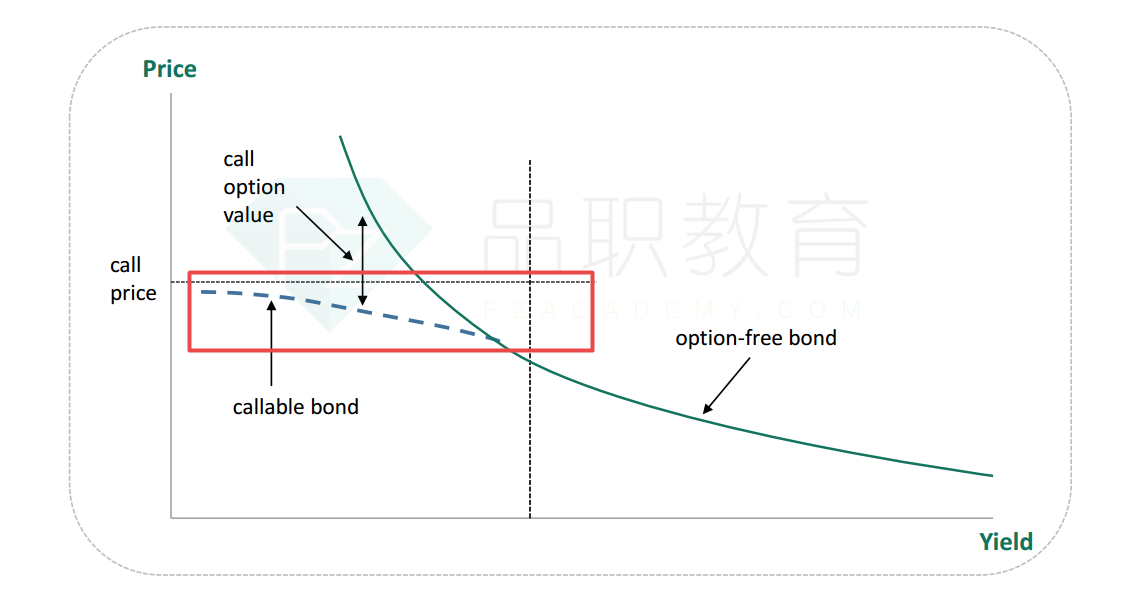

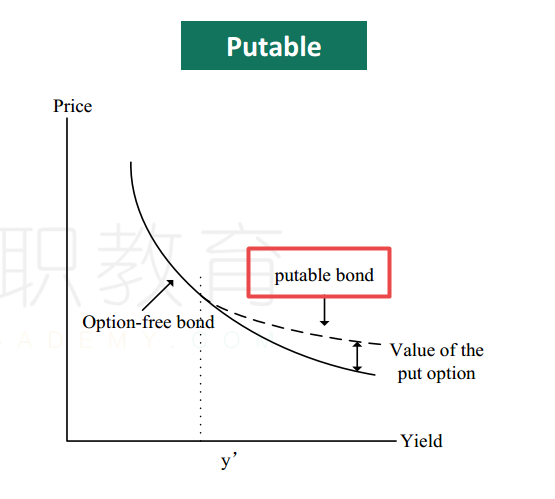

A callable bond is short an option, which creates negative convexity for some levels of interest rates. Regular bonds, as in answers C and D, have positive convexity, as well as puttable bonds.

解析:

从债券发行日到债券到期,下面哪一个债券有可能会出现负的凸性?

选B,因为callable bond即可赎回债券,对于债券购买人而言,赋予了发行方赎回债券的权利,那么债券的价格高到某一个程度的时候就不上去了,债券价格与利率变动呈现negative convexity的性质,这个是callable bond的特性。

有公式或者图形看出这四个选项的正负相关性吗