NO.PZ2018122701000046

问题如下:

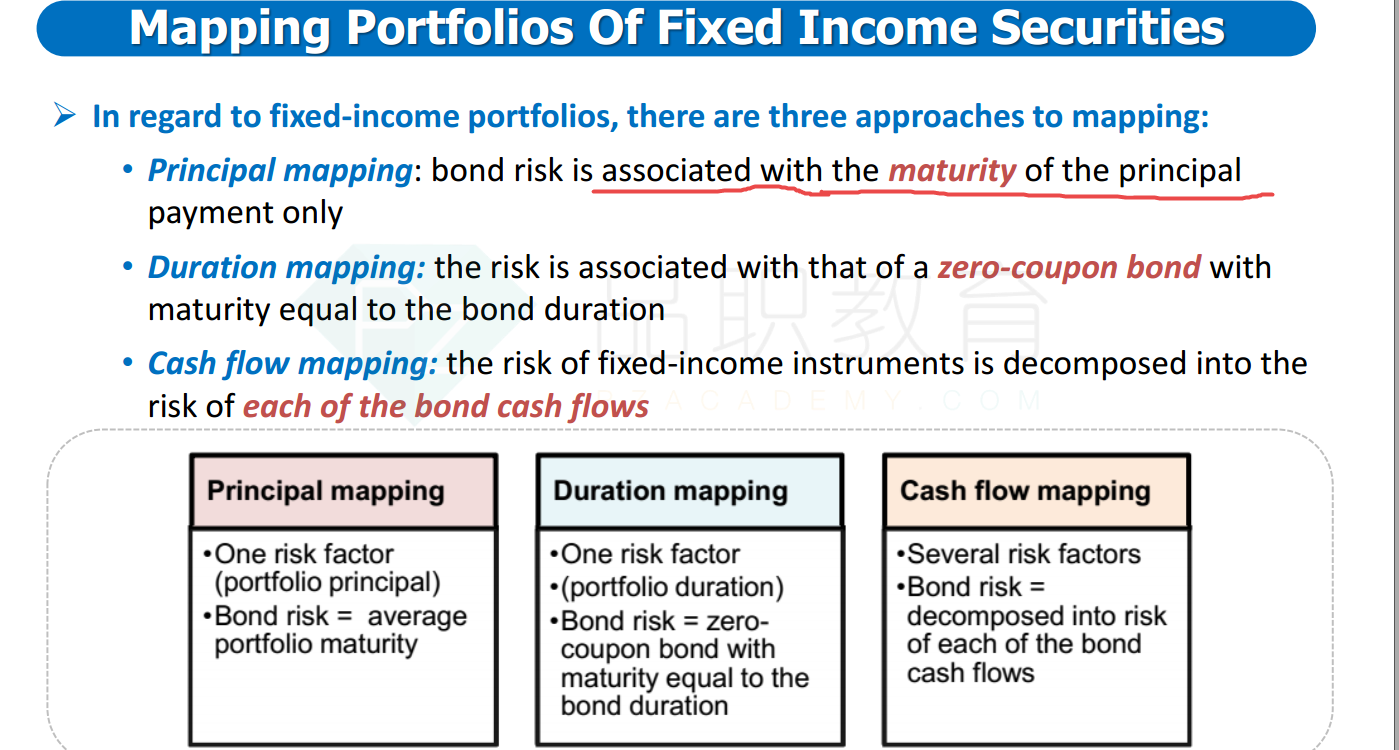

In fixed income portfolio mapping, when the risk factors have been selected, which of the following mapping approaches requires that one risk factor be chosen that corresponds to average portfolio maturity?

选项:

A.

Principal mapping

B.

Duration mapping

C.

Convexity mapping

D.

Cash mapping

解释:

A is correct.

考点Mapping to Fixed Income Portfolios

解析With principal mapping, one risk factor is chosen that corresponds to the average portfolio maturity. With duration mapping, one risk factor is chosen that corresponds to the portfolio duration. With cashflow mapping, the portfolio cashflows are grouped into maturity buckets. Convexity mapping is not a method of VaR mapping for fixedincome portfolios.

看不懂 老师能详细讲解一下吗?谢谢