NO.PZ2016082402000010

问题如下:

A and B are two perpetual bonds; that is, their maturities are infinite. A has a coupon of 4% and B has a coupon of 8%. Assuming that both are trading at the same yield, what can be said about the duration of these bonds?

选项: A. The duration of A is greater than the duration of B.

B.

The duration of A is less than the duration of B.

C.

A and B both have the same duration.

D.

None of the above.

解释:

ANSWER: C

Going back to the duration equation for the consol , , we see that it does not depend on the coupon but only on the yield. Hence, the durations must be the same. The price of bond A, however, must be half that of bond B.

解析:

A与B都是永续债券,他们的期限是无穷大的,A的coupon rate是4%,B的coupon rate是8%,假设yield相同,他们的duration?

选C,相同。永续年金的duration等于(1+y)/y。

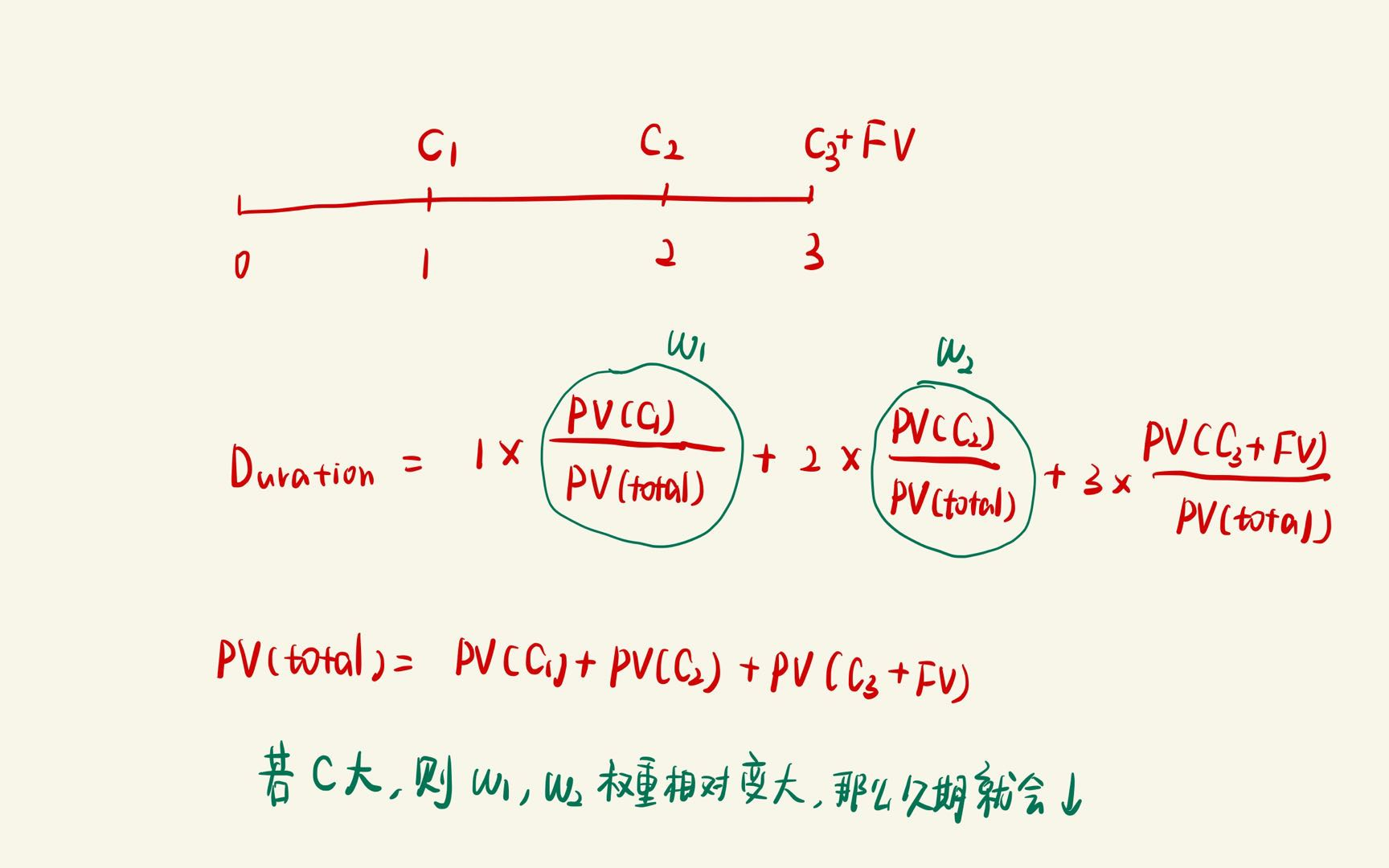

为什么一般债券coupon越高d越小