NO.PZ2020021002000107

问题如下:

In a perfect capital market, all stocks have the same risk premium. Is this statement consistent with CAPM? Explain

解释:

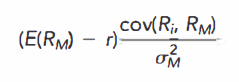

No, the risk premiums for different stocks will not be the same. It is, according to the CAPM:

where cov(Ri, RM) is the covariance between the returns of asset i and the returns of the market portfolio M.

中文解析:该观点与CAPM不符。按照CAPM,股票的风险溢价=(E(RM) - r)* Cov(Ri, RM) / σM2. 不同股票的风险溢价是不一样的。

风险溢价是rm-rf还是贝塔*(rm-rf)