NO.PZ2020011303000208

问题如下:

The term structure is initially flat at 5%, and an investor buys a five-year bond with a face value of USD 100 and a coupon of 4% at a spread of ten basis points. At the end of six months the term structure is flat at 6% and the spread is zero. Carry out a P&L decomposition.

解释:

First we calculate the carry roll-down. The cash-carry is 2%. In this case, the assumption underlying the carry roll-down is that the term structure remains flat at 5%. (This is true for all three definitions of carry roll-down.) The initial price paid for the bond is

![]()

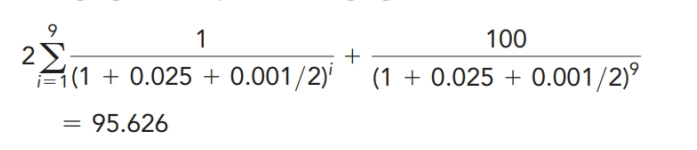

The price of the bond, if six months passes without rates changing or the spread changing, is

The carryroll-down is therefore: 2+95.626-95.199=2.427

This can alsobe calculated as 0.0255 × 95.199.

The value ofthe bond at the end of six months, assuming no spread change, is

After thespread change is considered, the value of the bond is![]()

This leads tothe following table

The bond price in six months is 92.214 and the investor receives a coupon of 2.000 just before

92.214 + 2.000-95.199 = ﹣0.985

The P&L decomposition splits this into:

(a) A carry roll-down of 2.427,

(b) The impact of a term structure change of -3.782, and

(c) A spread change of 0.370.

﹣0.985 = 2.427-3.782 + 0.370

题目问:利率的期限结构最开始时flat的,利率是5%,投资者买了一个5年期的债券,面值是100USD,coupon rate是4%,spread是10bp。在6个月结束的时候,利率的期限结构依旧是flat的,利率是6%,spread是0,请carry out P&L的分解。

题目默认半年付息一次。

首先计算5年期,coupon rate是4%,半年付息一次,YTM是(5%+0.1%)=5.1%,的债券的价格:

PMT=4%*100/2=2,I/Y=5.1%/2=2.55,N=5*2=10,FV=100

利用金融计算器求出PV=95.199

6个月之后,债券变成期限为4.5年,YTM=6%,其他条件不变的债券,这个债券的价格为:

PMT=2,I/Y=6%/2=3,N=4.5*2=9,FV=100

金融计算器求出PV=92.214

需要将95.199到94.214的这-0.985进行分解,看是由什么带来的:

1.如果利率和spread都不变,半年后债券的价值算出来是95.626,再加上2的利息,获得的收益就是carry roll-down 也就是2.427。

2.然后在1的基础上:如果利率变成6%,spread仍然保留也就是折现率用6.1%,求出来4.5年期的债券价值是91.844,也就是term structure变化造成的收益就是91.844-95.626 =-3.782

3.然后再2的基础上:如果利率是6%,spread没了,也就是spreadchange带来的收益就是92.214-91.844=0.37。

-0.985被拆解成了三个产生原因2.427 - 3.782 +0.37

请问整道题怎么理解呢?。。。。