NO.PZ2018111303000005

问题如下:

PZ company is an education company headquartered in China. It complies with IFRS. In 2018, PZ held a 20% passive equity ownership interest in T-internet company. At the end of the 2018, PZ company decides to increase its ownership interest to 50% on 1 January 2019 through a cash purchase. There are no intercompany transactions. The financial statement data for PZ company and T-internet company in the following table:

At the end of the 2019, assuming control and recognition of goodwill, PZ company’s Debt to Equity ratio is highest under which of the following accounting method:

选项:

A.Equity method.

B.full goodwill method.

C.partial goodwill method.

解释:

C is correct.

考点:不同的会计方法下对会计比率的影响

解析:首先在题干中已经说了是control over, 所以肯定不是equity method,排除A选项。

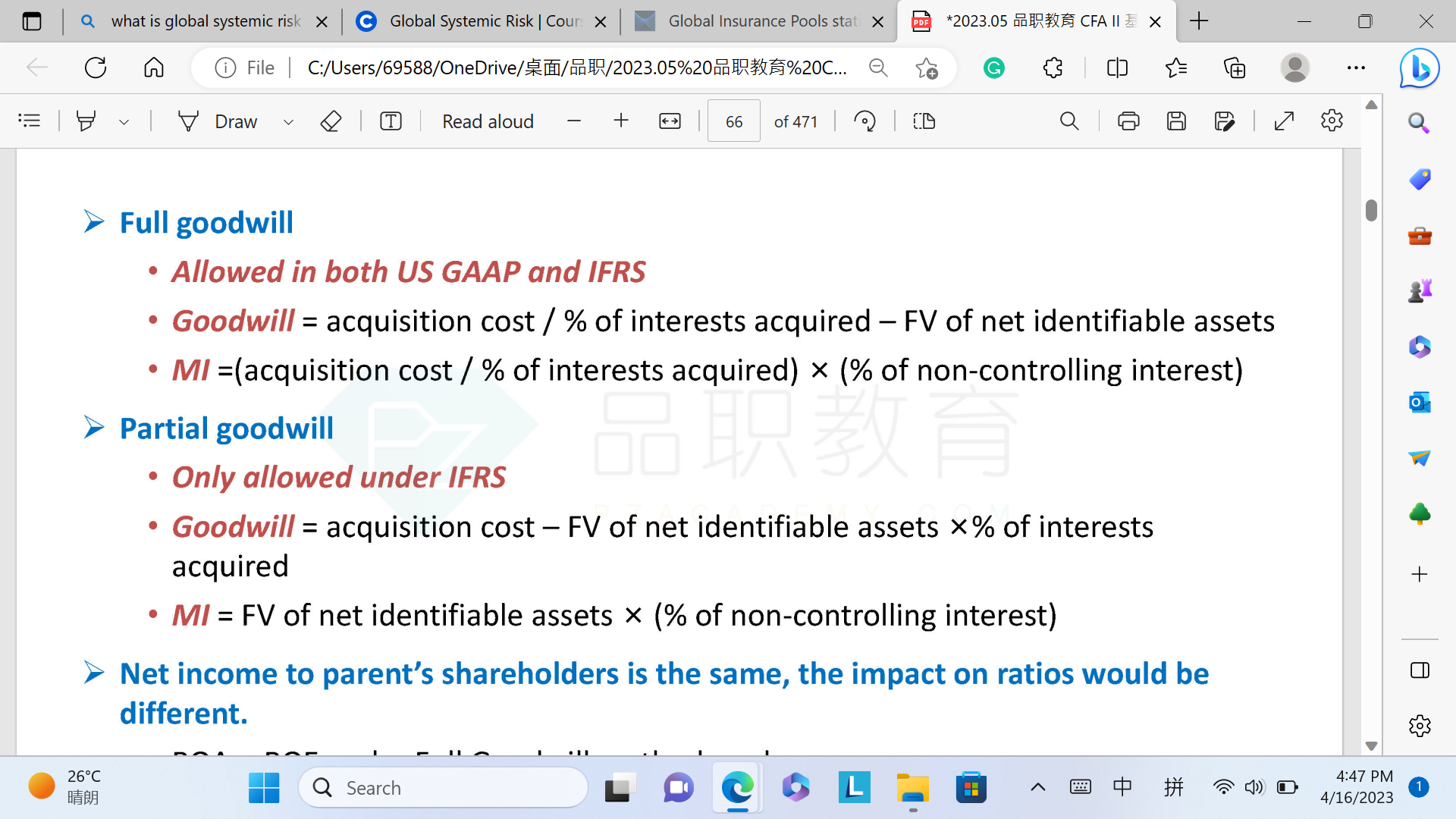

我们再来看B和C怎么选,在control的条件下,用acquisition Method。不管是full goodwill还是partial goodwill,在购买法下,首先都是将子公司的资产和负债合并过来的,然后再单列goodwill,所以它们的负债是一样的,资产方由于goodwill不同所以有区别。

因为购买法下是按100%比例合并子公司的资产和负债,然后抵消investment这一项的,这样就会使B/S不平衡,其相差的金额计为MI。

由于full goodwill和partial goodwill中计入的goodwill的金额不同,会导致资产的金额不同,所以就会导致MI不同,因此MI的大小是由goodwill的大小决定的。

如果并购产生了goodwill,那么full goodwill的金额肯定是大于partial goodwill,所以full goodwill下对应的MI就会比较大。

又因为MI计入在equity中,所以full goodwill的equity会比较大,分母大导致分数值变小,所以不选B,最后选C。

此题为例,full和partial分别算出来是0.8和1.08,对吧?